1

Affordable Housing

Frequently Asked Questions

Table Of Contents

1. Where are the Affordable Homes located? ............................................................................................ 3

2. What type of properties are available and how much will they cost? .................................................. 3

3. How does the Scheme work? ................................................................................................................... 4

4. Am I eligible for this scheme? .................................................................................................................. 4

5. How do I prove my right to reside indefinitely in the State? ................................................................. 5

6. How is purchasing power calculated? ..................................................................................................... 5

7. How will successful applicants be determined? ..................................................................................... 6

8. Am I eligible to apply if I am not a first-time buyer? .............................................................................. 6

9. How do I apply for the scheme? .............................................................................................................. 6

10. Do I need to be approved for a Mortgage in order to apply? .............................................................. 7

11. What documentation is needed to support my application? ............................................................... 7

Mandatory documentation required at the time of application............................................................ 7

Other Documentation (not mandatory at time of application but will be requested at a later date if

successful) ................................................................................................................................................. 8

12. What file types will be accepted on the application portal? ................................................................ 9

13. When will the properties be available?................................................................................................. 9

14. How much deposit do I need? ............................................................................................................. 10

15. If I am approved for the scheme, where can I source a loan? ............................................................ 10

16. How do I know which property to apply for? ..................................................................................... 10

2

17. What is the market value of the properties? ...................................................................................... 11

18. How is the affordable purchase price calculated? .............................................................................. 11

19. How is a decision made on my application? ....................................................................................... 12

20. If I am successful, will I be able to choose which house I want? ........................................................ 13

21. What is the Affordable Dwelling Contribution? .................................................................................. 13

22. What is the Affordable Dwelling Equity Share? .................................................................................. 13

23. What is a Redemption Payment? ........................................................................................................ 14

24. What is an Affordable Dwelling Purchase Agreement........................................................................ 14

3

1. Where are the Affordable Homes located?

Fingal County Council has agreed with the developer Manley Construction Ltd to sell fifty-two

affordable homes under the Affordable Housing Act 2021. The homes will be offered for sale to eligible

affordable housing applicants nominated by the Council. These homes are located in Hayestown,

Rush, Co. Dublin.

2. What type of properties are available and how much will they cost?

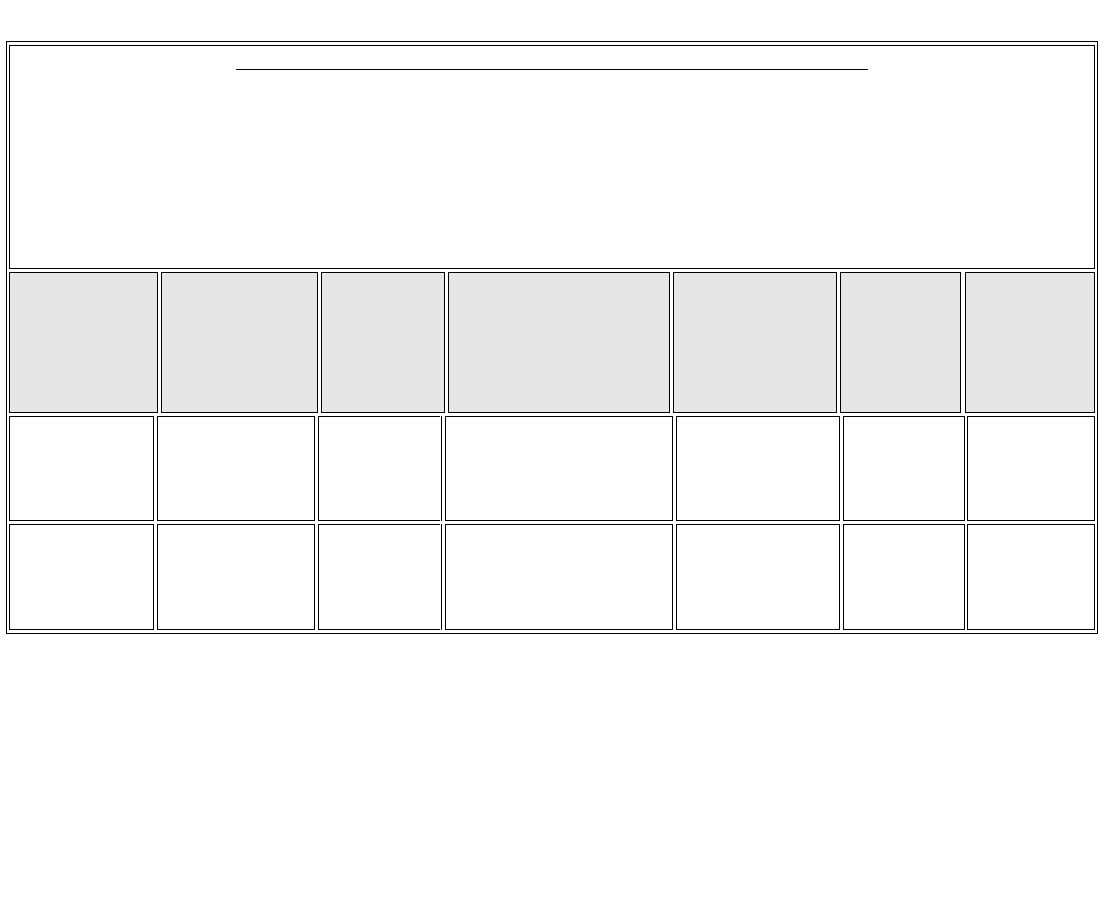

The table below lists the properties that are available. The cost of the 2-bedroom houses will start

from €228,000; the cost of the 3-bedroom houses will start from €284,500.

Property Type

Floor

Area

(m

2

)

Minimum Sale Price (€)

Approximate %

Reduction from

Market Value

Maximum Sale Price

(€)

(Based on a 15% - 16%

reduction from Market

Value)

2 Bedroom Mid

Terrace House

88

€228,000 - €230,000

21% - 22%

€245,000 - €248,000

2 Bedroom End of

Terrace House

79.2

€232,000

21% - 22%

€250,000

2 Bedroom semi-

detached House

79.2

€245,000

20% - 21%

€263,000

3 Bedroom Mid

Terrace House

98.2

€284,500 - €287,000

21% - 22%

€308,000 - €310,000

3 Bedroom End of

Terrace House

98.2

€284,500 - €298,000

20% - 22%

€308,000 - €320,000

3 Bedroom semi-

detached House

99.4

€299,500

21% - 22%

€320,000

See here for further information on the site plans and house types that are available.

4

3. How does the Scheme work?

The main points of the scheme are as follows:

• The scheme is for first time buyers who cannot afford to purchase a home at its market value.

*Some exceptions apply

• Applicants who are married, in a civil partnership or in a committed relationship with a partner

with whom he/she intends to live in the affordable dwelling, may not apply for an affordable

dwelling on his/her own but must apply jointly with his/her spouse/partner.

• To participate in the scheme, applicants will be required to maximise their mortgage

drawdown capacity (4 times a household income), from a participating lender or Local

Authority Home Loan. *Participating banks include AIB, Bank of Ireland, Permanent TSB &

Community Credit Union Limited.

• The maximum financial support (equity share) available on each home will be established by

Fingal County Council.

• All purchasers will sign up to an ‘Affordable Dwelling Purchase Agreement’ with Fingal County

Council. Under this agreement, the Council will take a percentage equity share in the dwelling,

equal to the difference between the market value of the dwelling and the price paid by the

purchaser.

• The equity share required will not be less than 15% of the market value of the dwelling.

• The purchaser can buy out this equity share at a time of their choosing but there will be no

requirement to do so.

• The Council may not seek realisation of its affordable dwelling equity for a 40-year period

(other than for breach of the agreement). However, the purchaser may choose to redeem or

buy out the affordable dwelling equity at any time by means of one or a series of payments to

the Council. The minimum amount of redemption payment is €10,000.

• If the purchaser chooses not to redeem the equity share while living in the home, the local

authority can do so when the property is sold or transferred, or after the death of the owner.

4. Am I eligible for this scheme?

In order to be eligible to apply for the scheme at Hayestown, applicants must satisfy the below criteria;

5

• Be a first-time buyer or meet the exceptions under the Fresh Start Principle, or own a

dwelling which, because of its size, is not suited to the current accommodation needs of the

applicant’s household.

• To apply for a 2-bedroom property, gross household income for the preceding 12 months

should be below €59,175. *Some exceptions apply

• To apply for a 3-bedroom property, gross household income for the preceding 12 months

should be below €72,000. *Some exceptions apply

• Each person included in the application must have the right to reside indefinitely in the State.

• The affordable home must be the household’s normal place of residence.

Further information on income that is assessable, including rules around overtime, bonuses and

commission, can be viewed here in the Income Assessment Policy Document.

5. How do I prove my right to reside indefinitely in the State?

For non-EU/EEA applicants, please submit a copy of your Irish Resident Permit (IRP) or GNI Stamp 4

card, indicating which stamp/permissions you have.

6. How is purchasing power calculated?

The purchasing power of applicants will be calculated as the combined total of:

• Maximum mortgage capacity, i.e., 4 times gross household income, plus,

• A minimum deposit of 10% of the affordable purchase price, plus,

• Relevant savings. *

*Where the applicant has savings or money not including the 10% deposit and an additional €30,000.

Eligibility Calculator

Hayestown Eligibility Income Calculations

6

7. How will successful applicants be determined?

As well as the above eligibility criteria, a Scheme of Priority for households deemed eligible will apply

to the scheme in the instance where there are more applicants than properties. The Scheme of Priority

can be read by clicking here.

8. Am I eligible to apply if I am not a first-time buyer?

Yes. Certain exemptions will apply under the Fresh Start Principle, including:

• Applicant(s) that previously held a legal interest in a residential property but is divested of this

legal interest through any of the following mechanisms may be eligible to apply’:

o Legal Separation

o Divorce

o Bankruptcy

o Insolvency

• Applicant(s) that previously owned, was beneficially entitled to, or have had an interest in a

dwelling in the state and that this dwelling, because of its size, is not suited to the current

accommodation needs of the applicant’s household i.e., an overcrowded house, may be

eligible to apply.

**Please note: If applying as a joint application, both applicants do not need to have the same Buyer Status.

One applicant can be a first-time buyer and the other can qualify under the Fresh Start Principle, however

both must also meet all the other eligibility criteria.

9. How do I apply for the scheme?

The application process will be via an online portal. The link to this online portal is available here and

will be available and live from the 13

th

of June at 12pm. The system will allow for the input of all

relevant data and uploading of all supporting documentation.

In the online application process, applicants will have to:

• provide personal details (e.g., name, address, date of birth, PPSN),

7

• confirm that they are a First-Time Buyer or that they qualify under the Fresh Start Principle,

• declare the total gross annual income for their household for the preceding 12 months,

• provide evidence of their 10% deposit and any savings, i.e., bank statements,

• provide evidence of how they intend to Finance the property, i.e., mortgage approval-in-

principle or a mortgage calculator clearly showing household income.

• Proof that you have the right to reside indefinitely in the State.

Supporting documentation will be required before an applicant is approved for the purchase of an

affordable home. All application details and data submitted will only be retained for this scheme and

will not be carried forward for any future affordable housing scheme(s).

Applicants who submit multiple applications and/or include any false or misleading

information on their application will be disqualified from this process.

10. Do I need to be approved for a Mortgage in order to apply?

Although it is not a requirement, it is recommended that applicants have their Mortgage Approval in

Principle prior to applying for this scheme or at least be in a position to apply for a mortgage.

11. What documentation is needed to support my application?

Mandatory documentation required at the time of application

1. Proof of Income Documentation required:

o If EMPLOYED, please provide an Employment Detail Summary (previously known as P60)

which is available via www.revenue.ie/MyAccount. Please also arrange to have this Salary

Certificate completed by your employer. Payslips are NOT acceptable evidence.

8

o If SELF EMPLOYED, please upload Accountants Report/Audited Accounts (2 Years

Required), Current Tax Balancing Statement & Current Preliminary Revenue Tax Payment

Receipt.

o If NOT EMPLOYED, please upload Statement of total benefits received from Social Welfare

which can be requested via email from your local Social Welfare/Intreo office.

2. Proof of Citizenship:

o Passport or Birth Certificate

3. Proof of the Right to Reside in Ireland (if applicable):

o For non-EU/EEA applicants, please submit a copy of your Irish Resident Permit (IRP) or

GNI Stamp 4 card, indicating which stamp/permissions you have.

4. Evidence of Ability to Finance the Purchase:

o A mortgage letter of approval in principle from a Bank / Building Society / Local Authority

stating the maximum mortgage available to applicant(s)

or

o Photograph/screen shot of the use of an on-line mortgage calculator from any lending

institution to demonstrate your ability to finance the purchase. Applicant(s) must apply for

the maximum mortgage available to them.

and

o Proof of savings and deposit in the form of a current bank statement on headed paper

dated within the last 3 months (If applicable, please include proof of Help-to-Buy).

Other Documentation (not mandatory at time of application but will be requested at a

later date if successful)

1. Proof of Buyer Status:

9

For First Time Buyers –

o Confirmation of eligibility for Help to Buy Scheme: Print out from Revenue portal

(myAccount for PAYE applicants / ROS for Self-assessed applicants) confirming names

of applicant(s) and maximum entitlement under the scheme.) *Note that applicants

are considered first-time-buyers only if BOTH are buying their home for the first time.

2. Proof of Residency in Fingal Administrative area for a minimum period of 5 years, for

applicants to qualify under the 30% Residency Rule (provide a series of any of the

following documents spanning 5 years)

o Series of utility bills

o Bank/Credit Union statements

o Any official dated documentation showing your address

12. What file types will be accepted on the application portal?

The portal will accept the following image files:

• PDF,

• JPEG,

• PNG.

Editable documents such as Word (.doc), or Excel (.xls) are not accepted.

13. When will the properties be available?

• Phase 1, which consists of 24 units is due to be completed in Quarter 1, 2024.

• Phase 2, which consists of 18 units is due to be completed in Quarter 2, 2024.

• Phase 3, which consists of 10 units is due to be completed in Quarter 3, 2024.

10

14. How much deposit do I need?

Financial institutions require that a minimum 10% deposit must be raised by purchasers.

Example:

For a property with a purchase price of €280,000 you will need a deposit of at least €28,000.

The Help to Buy Scheme will be acceptable as part of your 10% deposit.

15. If I am approved for the scheme, where can I source a loan?

Finance can be secured from any lending institution i.e., a bank, building society. Alternatively, finance

can be sourced via Fingal County Council by way of a Local Authority Home Loan. Please see

https://www.fingal.ie/localauthorityhomeloan for further information.

16. How do I know which property to apply for?

The property being applied for must be within the applicant’s affordability range and must also suit

the household’s housing need in line with the Scheme of Priority. The priority as to which type of

dwelling is deemed to adequately cater to the accommodation needs of a household, will be made on

the following basis:

Dwelling Type

Meets accommodation needs of:

Three-bedroom dwelling

2 or more-person household

Four-bedroom dwelling

3 or more-person household

Full information can be found in the Scheme of Priority, which can be viewed by clicking here.

11

17. What is the market value of the properties?

The market value of an affordable home is the price for which the affordable home might reasonably

be expected to achieve on the open market. The market value of the properties in Hayestown are

below:

• Type H10 & H12 – 2-bedroom house: Between €290,000 and €310,000

• Type H1 & H8 – 3-bedroom house: Between €362,500 and €380,000

18. How is the affordable purchase price calculated?

Fingal County Council, in line with the Affordable Housing Regulations, will set a minimum price that

the affordable properties can be sold for. The affordable purchase price to be paid by an applicant

will all depend on that applicant’s purchasing power and their ability to raise the relevant finances.

Worked Example Based on Hayestown 3 Bed Mid Terrace House

The below example shows varying incomes and how they determine the affordable purchase price and the Council’s

equity share of a property with a market value of €362,500.

These examples are based on the minimum market value for a 3-bed mid terrace house in the Hayestown scheme

in Rush.

Gross

household

income

Mortgage

Capacity

(income x 4)

Deposit (Min.

10%)

Applicant Purchase

Price (Mortgage +

Deposit)

FCC

Contribution

Equity

Share

Total Cost

€65,000

€260,000

€28,889

€288,889

€73,611

20.31%

€362,500

€69,000

€276,000

€30,667

€306,667

€55,833

15.40%

€362,500

12

Worked Example Based on Hayestown 2 Bed Mid Terrace House

The below example shows varying incomes and how they determine the affordable purchase price and the Council’s

equity share of a property with a market value of €290,000.

These examples are based on the minimum market value for a 2-bed mid terrace house in the Hayestown scheme

in Rush.

Gross

household

income

Mortgage

Capacity

(income x 4)

Deposit

(Min. 10%)

Applicant Purchase

Price (Mortgage +

Deposit)

FCC

Contribution

Equity

Share

Total Cost

€52,000

€208,000

€23,111

€231,111

€58,889

20.31%

€290,000

€55,000

€220,000

€24,444

€244,444

€45,556

15.71%

€290,000

*The higher an applicant’s purchasing power is, the more they will contribute to the price and the less

equity the Council will take.

* The above examples are indicative only. There are some cases where significant savings can add to

purchasing power where gross income is lower.

19. How is a decision made on my application?

The decision on your application is made by Fingal County Council in accordance with the eligibility

criteria, time and date of applications and the Council’s Scheme of Priority. Homes will be allocated

on a First-Come, First-Serve basis.

13

20. If I am successful, will I be able to choose which house I want?

If you are successful, and after you have received your offer letter from Fingal County Council, your

details will be passed over to the Developer. The preference of applicants for a particular house type

& location within the scheme will be based on the confirmed order of merit following the assessment

of applications by Fingal County Council.

When your property is assigned, you will be required to pay a booking deposit.

All successful applicants will be required to obtain independent legal advice and pay their own legal

costs to process the sale of the property. These and other associated costs must be considered when

applying.

21. What is the Affordable Dwelling Contribution?

The Affordable Dwelling Contribution is the amount paid by Fingal County Council towards your

purchase of an affordable home. This refers to the monetary amount that the Council will pay.

The Affordable Dwelling Contribution is the difference between the combined total of the purchaser’s

deposit, maximum mortgage capacity and savings where relevant and the market value of the home

as per date of offer.

22. What is the Affordable Dwelling Equity Share?

The Equity Share is simply the contribution that the Council provide expressed as a percentage.

It is the percentage of the market value that Fingal County Council will contribute to the purchase of

the affordable property. This will be at least 15% of the market value. This entitles the Council to the

same percentage in value of a future sale of the property subject to terms and conditions. It does not

establish the Council as a co-owner of the property.

14

23. What is a Redemption Payment?

A Redemption Payment is a payment that is made by the Purchaser to Fingal County Council to pay

back the Affordable Dwelling Contribution that was provided. Redemption Payments are subject to

certain conditions which are outlined in the Affordable Dwelling Purchase Agreement. The minimum

redemption payment is €10,000. The purchaser can redeem or ‘buy out’ the equity share at a time of

their choosing, but there is no obligation to do so. If the purchaser chooses not to redeem the equity

share while living in the home, the Council can do so when the property is sold, transferred, or after

the death of the owner.

24. What is an Affordable Dwelling Purchase Agreement

The Affordable Dwelling Purchase Agreement is the legal contract between the Council and the

purchaser setting out the terms and conditions under which the Council provides the Affordable

Dwelling Contribution.

Each successful applicant will enter into an Affordable Dwelling Purchase Agreement with Fingal

County Council. This will be prior to or at the same time as the closing of the purchase of their

affordable home. The agreement covers the obligations of the purchaser and the Council and makes

provision for the registration of the agreement with the Registry of Deeds/Land Registry. The

agreement will also set out how and when the homeowner can make redemption payment(s) to

reduce the Council’s affordable dwelling equity share as well as the conditions under which the

Council may seek redemption of the affordable dwelling equity.

Successful applicants will be required to enter into a Contract for Sale with the developer in order to

complete the purchase of the affordable home. This Contract for Sale will include all standard

conveyancing terms and conditions.

Applicants should note that giving untrue/incorrect information on their application may lead to

the Affordable Dwelling Purchase Agreement being terminated and the offer to purchase being

withdrawn.