I am grateful to Clare Macallan, Daisy McGregor and James Benford for their assistance in preparing

these remarks, and to Nishat Anjum, Ambrogio Cesa-Bianchi, Alex Haberis, James O’Connor and

Carlos van Hombeeck for background research and analysis.

All speeches are available online at www.bankofengland.co.uk/news/speeches

1

The Growing Challenges for Monetary Policy in the current

International Monetary and Financial System

Speech given by

Mark Carney

Governor of the Bank of England

Jackson Hole Symposium 2019

23 August 2019

All speeches are available online at www.bankofengland.co.uk/news/speeches

2

2

Introduction

Before turning to the focus of my remarks, I would like to begin with a few comments on the UK outlook.

A snapshot suggests the UK economy is currently close to equilibrium, operating just below

potential with inflation just above its target.

Both headline and core inflation are around 2%, and domestic price pressures have been picking up notably.

In particular, the labour market is tight. Growth in wages and unit wage costs have strengthened

considerably as slack has been absorbed, with both now running at their highest rates in over a decade.

The strength of the labour market is supporting consumer spending, which is rising broadly in line with real

incomes.

But pictures can deceive; two large, volatile forces could push the UK economy far from balance.

Until the start of this year, the UK economy had been growing around its trend rate. Since then, the

intensification of Brexit uncertainties and weaker global activity have weighed heavily on UK activity.

Global momentum remains soft, despite the broad-based easing in monetary policy expectations. In part this

reflects a significant spike in economic policy uncertainty and the related risk that protectionism could prove

more pervasive, persistent and damaging than previously expected. As I will discuss in a moment, these

headwinds are now restraining business investment globally and could push down on the global equilibrium

interest rate, exacerbating concerns about limited monetary policy space.

Long-term government bond yields have fallen sharply alongside the falls in expected policy rates. US 10-

year yields are near three-year lows, and 10-year gilt yields and German 10-year bund yields are their lowest

ever. Around $16 trillion of global debt is now trading at negative yields.

As material as these global developments are, the UK outlook hinges on the nature and timing of Brexit.

The UK economy contracted slightly last quarter and surveys point to stagnation in this one. Looking

through Brexit-related volatility, it is likely that underlying growth is positive but muted.

The biggest economic headwind is weak business investment, which has stagnated over the past few years,

despite limited spare capacity, robust balance sheets, supportive financial conditions and a highly

competitive exchange rate. There is overwhelming evidence that this is a direct result of uncertainties over

the UK’s future trading relationship with the EU, and it serves as a warning to others of the potential impact

of persistent trade tensions on global business confidence and activity.

The UK economy could follow multiple possible paths depending on how Brexit progresses with

material implications for the stance of monetary policy.

In recent weeks, the perceived likelihood of No Deal has risen sharply as evidenced by betting odds and

financial market asset pricing (the UK now has the highest FX implied volatility, the highest equity risk

premium and lowest real yields of any advanced economy).

In the event of a No Deal No Transition Brexit, sterling would probably fall, pushing up inflation, and demand

would weaken further, reflecting lost trade access, heightened uncertainty and tighter financial conditions.

Unusually for an advanced economy slowdown, there would also be a large, immediate hit to supply. The

Monetary Policy Committee (MPC) would need to assess to what extent that reflects temporary disruption to

All speeches are available online at www.bankofengland.co.uk/news/speeches

3

3

production, with limited implications for inflation in the medium term, or a fundamental destruction of supply

capacity because of the abrupt change in the UK’s economic relationship with the EU.

As the MPC has repeatedly emphasised, the monetary policy response to No Deal would not be automatic

but would depend on the balance of these effects – on demand, supply and the exchange rate – on medium

term inflationary pressures. In my view, the appropriate policy path would be more likely to ease than not,

using the flexibility in the MPC’s remit to lengthen the period over which inflation is returned to target. But

much would depend on the exact nature of No Deal and its impact. In the end, monetary policy can only

help smooth the adjustment to the major real shock that an abrupt No Deal Brexit would entail, but even its

ability to do that would be constrained by the limits to the MPC’s tolerance of above target inflation.

While the possibility of No Deal has increased, it is not a given. Along another path, it is possible that

domestic political events or negotiations with the EU could lead to a longer period of uncertainty over the

eventual future relationship, even in the event that an agreement is struck. On past performance, the longer

these uncertainties persist, the more likely it is that growth will remain below potential raising the prospect of

both softer domestically generated inflation and resurgent imported inflation if recent sterling weakness were

to endure. Once again, the MPC would need to weigh the opposing forces when setting policy.

Finally, some form of agreement remains possible. After all, that is the avowed preference of both the UK

and EU. In this event, consistent with the MPC’s most recent projections, as details of the future relationship

gradually emerge, business investment recovers and household spending picks up, resulting in excess

demand and inflationary pressures gradually building. In the Committee’s judgment, this path for the

economy would likely require limited and gradual interest rate increases.

The coming months could be decisive. If there are material Brexit developments, the MPC will transparently

assess their implications and set policy to achieve the 2% inflation target in a sustainable manner.

I. Challenges for Monetary Policy in the current IMFS

When Ben Bernanke was retiring from the Fed, his closing remarks to central bank governors at the BIS set

us the task of sorting out the deep flaws in the international monetary and financial system (“IMFS”). Six

years later, with my demise as governor on the horizon, I’m going to ‘pay it forward’ by focusing on how the

nature of the IMFS challenges monetary policy.

For decades, the mainstream view has been that countries can achieve price stability and minimise

excessive output variability by adopting flexible inflation targeting and floating exchange rates. The gains

from policy coordination were thought to be modest at best, and the prescription was for countries to keep

their houses in order.

1

This consensus is increasingly untenable for several reasons. Globalisation has steadily increased the

impact of international developments on all our economies. This in turn has made any deviations from the

core assumptions of the canonical view even more critical. In particular, growing dominant currency pricing

(DCP) is reducing the shock absorbing properties of flexible exchange rates and altering the inflation-output

volatility trade-off facing monetary policy makers. And most fundamentally, a destabilising asymmetry at the

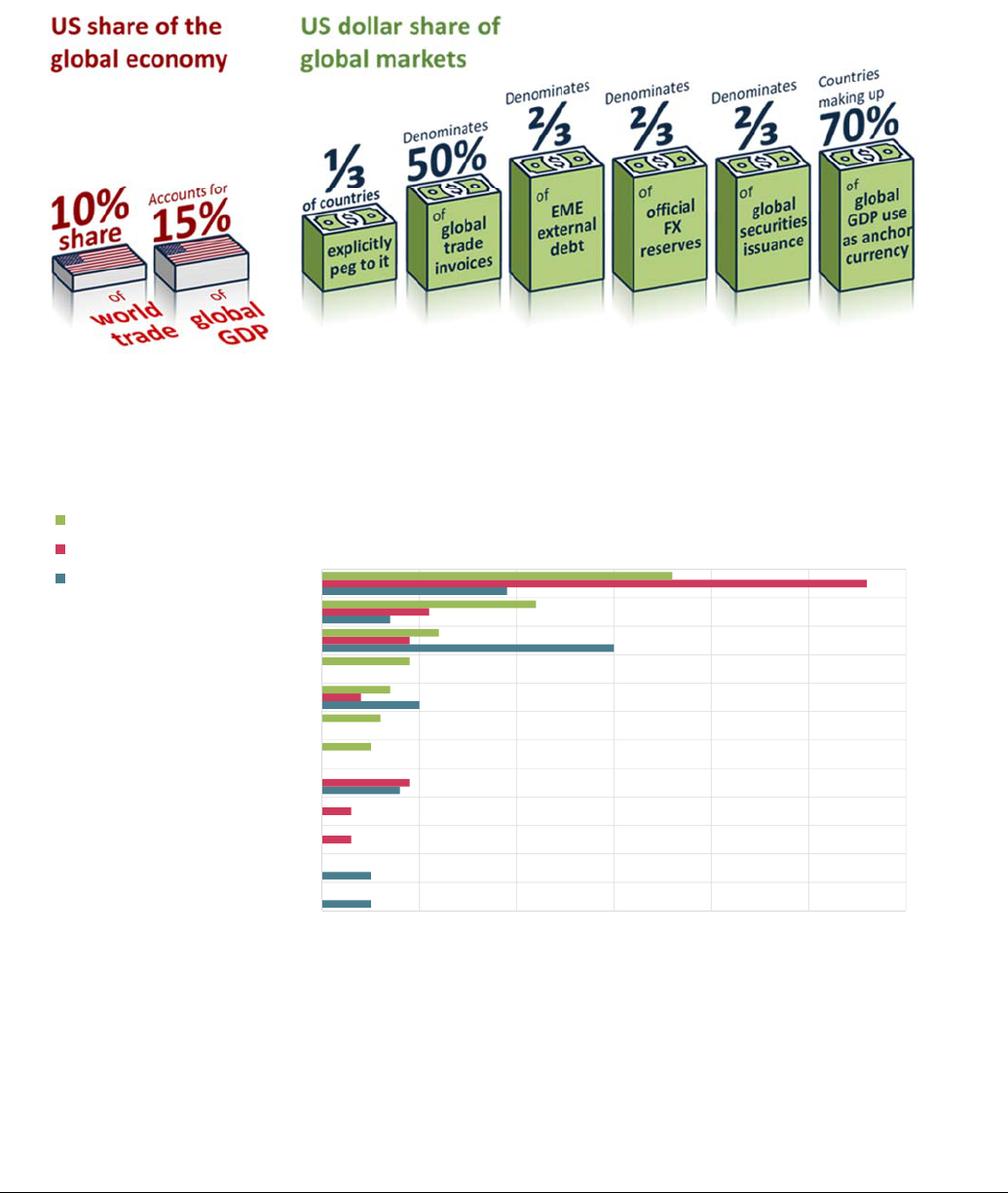

heart of the IMFS is growing. While the world economy is being reordered, the US dollar remains as

important as when Bretton Woods collapsed (Figure 1).

1

This view is summarised in a speech by John Murray, ‘With a Little Help from Your Friends: The Virtues of Global Economic

Coordination’, 29 November 2011.

All speeches are available online at www.bankofengland.co.uk/news/speeches

4

4

The combination of these factors means that US developments have significant spillovers onto both the trade

performance and the financial conditions of countries even with relatively limited direct exposure to the US

economy.

These dynamics are now increasing the risks of a global liquidity trap. In particular, the IMFS is structurally

lowering the global equilibrium interest rate, r*, by:

- feeding a global savings glut, as EMEs defensively accumulate reserves of safe US dollar assets

against the backdrop of an inadequate and fragmented global financial safety net;

- reducing the scale of sustainable cross border flows, and as a result lowering the rate of global

potential growth; and

- fattening of the left-hand tail and increasing the downside skew of likely economic outcomes.

In an increasingly integrated world, global r* exerts a greater influence on domestic r*.

2

As the global

equilibrium rate falls, it becomes more difficult for domestic monetary policy makers everywhere to provide

the stimulus necessary to achieve their objectives.

These dynamics are directly relevant to the current risks of a global slowdown. At present, there are

relatively few fundamental imbalances in terms of capacity constraints or indebtedness that would of

themselves portend a recession.

3

However, the combination of structural imbalances at the heart of the

IMFS itself and protectionism are threatening global momentum.

The amplification of spillovers by the IMFS matters less when the global expansions are relatively

synchronised or when the US economy is relatively weak. But when US conditions warrant tighter policy

there than elsewhere, the strains in the system become evident.

These conditions emerged last year. US fiscal policy had boosted growth at a time when the US economy

was near full employment. US monetary policy had to tighten consistent with the Fed’s dual mandate. The

resulting dollar strength and financial spillovers tightened financial conditions in most other economies by

more than was warranted by their domestic conditions (two thirds of the global economy was growing at

below potential rates at the start of 2019, and that proportion has since risen to five sixths). More recently,

the dramatic increase in trade tensions (Chart 1) has reinforced their effects by increasing risk premia.

Today, the combination of heightened economic policy uncertainty (Chart 2), outright protectionism and

concerns that further, negative shocks could not be adequately offset because of limited policy space is

exacerbating the disinflationary bias in the global economy.

What then must be done?

In the short term, central bankers must play the cards they have been dealt as best they can.

That means using the full flexibility in flexible inflation targeting. To retain the essential credibility of their

frameworks, this is best done transparently with central bankers explaining their reasons for targeting

specific trade-offs between price stability and output volatility.

2

See ‘[De]Globalisation and Inflation’, 2017 IMF Michel Camdessus Central Banking Lecture given by Mark Carney, 18 September

2017.

3

See ‘The Global Outlook’, speech by Mark Carney, 12 February 2019.

All speeches are available online at www.bankofengland.co.uk/news/speeches

5

5

Those at the core of the IMFS need to incorporate spillovers and spill backs, as the Fed has been doing.

More broadly, central banks need to develop a better shared understanding of the scale of global risks and

their consequences for monetary policy.

We cannot all export our way out of these challenges. In a global liquidity trap, there are gains from

coordination, and other policies – particularly fiscal – have clear roles to play. And acting earlier and more

forcefully will increase their effectiveness.

In the medium term, policymakers need to reshuffle the deck.

That is, we need to improve the structure of the current IMFS. That requires ensuring that the institutions at

the heart of market-based finance, particularly open-ended funds, are resilient throughout the global financial

cycle. It requires better surveillance of cross border spillovers to guide macroprudential and, in extremis,

capital flow management measures. And it underscores the premium on re-building an adequate global

financial safety net.

In the longer term, we need to change the game. There should be no illusions that the IMFS can be

reformed overnight or that market forces are likely to force a rapid switch of reserve assets.

4

But equally

blithe acceptance of the status quo is misguided. Risks are building, and they are structural. As Rudi

Dornbusch warned, “In economics, things take longer to happen than you think they will, and then they

happen faster than you thought they could”.

When change comes, it shouldn’t be to swap one currency hegemon for another. Any unipolar system is

unsuited to a multi-polar world. We would do well to think through every opportunity, including those

presented by new technologies, to create a more balanced and effective system.

II. Growing Challenges in the Current IMFS

The structure of the current international monetary financial system is making it increasingly difficult for

monetary policy makers to achieve their domestic mandates to stabilise inflation and maintain output at

potential.

According to the mainstream view, these objectives are best achieved through operationally independent

central banks adopting flexible inflation targeting and allowing their exchange rates to float.

That view rests on two pillars. The first is that floating exchange rates are effective absorbers of global

shocks, insulating domestic employment and output from developments abroad. If import prices are fully

flexible and international financial markets are complete, then changes in exchange rates pass through fully

to import prices, and the optimal monetary policy response is to accommodate the effect on inflation, keeping

output close to potential and the price of domestic output stable.

5

That leads directly to the second pillar – that there are only modest gains from international policy

cooperation and coordination in such circumstances. This long-standing and widely held view reflects the

4

The analysis of Gita Gopinath, Emmanuel Farhi, Matteo Maggiori and Jeremy Stein, amongst others, emphasises the persistence in

the structure of the current IMFS.

5

See Corsetti, G, Dedola, L, and Leduc, S (2010), ‘Optimal Monetary Policy in Open Economies’, Handbook of Monetary Economics,

Vol. 3, Chapter 16, pp. 861-933; and Benigno, G and Benigno, P (2006), ‘Designing targeting rules for international monetary policy

cooperation’, Journal of Monetary Economics, Vol. 53(3), pp. 473-506. In the standard welfare-based analyses of optimal monetary

policy in an open economy, a key consideration is the extent to which sticky prices in different currencies lead to deviations from the law

of one price (LOOP) for different goods. The first-best (efficient) outcome is for goods to sell for the same price when converted into

different currencies. If this is not the case, demand is misaligned internationally, which in turn creates an inefficient allocation of factor

inputs. Under PCP, the full flexibility of import prices means the exchange rate can act as an efficient shock absorber, adjusting to

ensure that the LOOP holds.

All speeches are available online at www.bankofengland.co.uk/news/speeches

6

6

beliefs that any externalities that might exist are almost trivially small and that trying to address them would

be fine-tuning to the n

th

degree.

The mainstream view is increasingly anachronistic for several reasons.

First and foremost, international linkages have risen dramatically over the past few decades, increasing the

importance of cross border spillovers.

6

Growing cross border trade means external demand has greater effects on domestic resource allocation and

therefore inflation. The integration of low-cost producers into the global economy has imparted a steady

disinflationary bias through its direct effect on prices. The expansion in global value chains has increased

the synchronisation of producer prices across countries. Financial linkages have increased leading to a

faster and more powerful transmission of shocks across countries. And globalisation has increased the

contestability of markets, weakening the extent to which slack in domestic labour markets influences

domestic inflationary pressures.

7

Second, the changing nature of trade invoicing is affecting import price pass through and changing the

inflation-output volatility trade-off facing monetary policy makers.

Dominant currency pricing is widespread (partly due to the growth of supply chains), leading to deviations

from the law of one price and misalignments in countries’ terms of trade.

8

The dollar represents the currency

of choice for at least half of international trade invoices, around five times greater than the US’s share in

world goods imports, and three times its share in world exports.

9

The resulting stickiness of import prices in dollar terms means exchange rate pass-through for changes in

the dollar is high regardless of the country of export and import, while pass-through of non-dominant

currencies is negligible. As a result, import prices do not adjust efficiently to reflect changes in relative

demand between trading partners, in part because expenditure switching effects are curtailed,

10

and global

trade volumes are heavily influenced by the strength of the US dollar.

11

This is less of a problem when all boats are rising with the global tide of synchronised growth. But when the

tide is rising in America while receding elsewhere, those authorities face more difficult trade-offs between

price stability and output volatility – a situation that could create large potential gains from policy coordination

that independent policymakers would not address.

6

World trade as a share of global GDP has doubled since 1970. Over the past two decades, 80% of the increase in total trade has

come from intermediates goods trade, driving up the value added of imports as a share from 10% of exports in 1990 to around 20% in

2015. Cross-holding of countries’ assets and liabilities increased almost fourfold since 1990, and measures of stock market integration

are at their highest ever (see Bastidon, C, Bordo, M, Parent, A, and Weidenmier, M (2019), ‘Towards an Unstable Hook: The Evolution

of Stock Market Integration Since 1913’, NBER Working Paper No. 26166.

7

For more detail on these changes, see ‘[De]Globalisation and Inflation’, ibid.

8

Dominant currency pricing refers to the widespread use of a single currency – the US dollar – in trade invoicing, in place of the

currency of either the producer or the importer. Import prices will therefore depend on changes in the bilateral exchange rate between

the local and the dominant currency, rather than that between the local and producer currency. For evidence, see Goldberg, L and Tille,

C (2009), ‘Macroeconomic interdependence and the international role of the dollar’, Journal of Monetary Economics, 56 (7), pp. 990-

1003; and Gopinath, G(2016). “The International Price System,” Jackson Hole Symposium Proceedings.

9

Gopinath (2016), ibid, and Ito, H, and Kawai, M (2016), ‘Trade Invoicing in Major Currencies in the 1970s-1990s: Lessons for

Renminbi Internationalization’, Journal of the Japanese and International Economies, Volume 42, pp. 123–145.

10

For a country with a large share of trade invoiced in dollars, a depreciation against the dollar raises the domestic price of imports,

causing domestic households and firms to switch their expenditure away from foreign goods. But it leaves the (dollar) price of exports in

the markets in which they are sold unchanged, albeit making them more profitable for domestic exporters in terms of home currency.

Because imports would fall straight away and it would take time for the export sector to expand to take advantage of the higher profits, it

is therefore likely that a rebalancing of the economy from imports to exports would be slower than if traded goods were priced in the

currencies of their production. In addition, other things equal, the rise in import prices would lead to a pick-up in imported inflationary

pressure.

11

Boz, Gopinath and Plagborg-Moller (2017) show that a 1% appreciation of the dollar leads, all else equal, to a 0.6% contraction in

trade volumes in the rest of the world.

All speeches are available online at www.bankofengland.co.uk/news/speeches

7

7

Third, a growing asymmetry at the heart of the IMFS is putting the global economy under increasing strain.

Huge network effects mean the dollar has remained dominant in the IMFS despite the transformation of the

global economy. At the time of the Latin American debt crisis, EMEs made up a little more than one third of

global GDP. Since the last Fed tightening cycle, their share of global activity had risen from around 45% to

60%. By 2030, it is projected to rise to around three quarters.

As well as being the dominant currency for the invoicing and settling of international trade, the US dollar is

the currency of choice for securities issuance and holdings, and reserves of the official sector. Two-thirds of

both global securities issuance and official foreign-exchange reserves are denominated in dollars.

12

The

same proportion of EME foreign currency external debt is denominated in dollars

13

and the dollar serves as

the monetary anchor in countries accounting for two thirds of global GDP.

14

The US dollar’s widespread use in trade invoicing and its increasing prominence in global banking and

finance are mutually reinforcing. With large volumes of trade being invoiced and paid for in dollars, it makes

sense to hold dollar-denominated assets. Increased demand for dollar assets lowers their return, creating an

incentive for firms to borrow in dollars. The liquidity and safety properties encourage this further.

15

In turn,

companies with dollar-denominated liabilities have an incentive to invoice in dollars, to reduce the currency

mismatch between their revenues and liabilities. More dollar issuance by non-financial companies and more

dollar funding for local banks makes it wise for central banks to accumulate some dollar reserves.

Given the widespread dominance of the dollar in cross border claims, it is not surprising that developments in

the US economy, by affecting the dollar exchange rate, can have large spillover effects to the rest of the

world via asset markets. As Hélène Rey has put it,

16

and as Arvind Krisnamurthy and Hanno Lustig echo in

their paper for this symposium, the global financial cycle is a dollar cycle.

In part, that arises because movements in the US dollar significantly affect the real burden of debt for those

companies (especially in EMEs) that have borrowed unhedged in dollars, and tend to reduce the dollar value

of companies’ collateral.

17

Both result in tighter credit conditions and, in the extreme, defaults.

Fluctuations in the dollar also significantly affect the risk appetite of global investors. As discussed by

Şebnem Kalemli-Özcan earlier today, these risk spillovers can have a significant impact on receiving

economies, especially in EMEs where global risk perceptions interact with country-specific risks.

For EMEs, this manifests in volatile capital flows that amplify domestic imbalances and leave them more

vulnerable to foreign shocks (Charts 3 and 4). One fifth of all surges in capital flows to EMEs have ended in

financial crises, and EMEs are at least three times more likely to experience a financial crisis after capital

flow surges than in normal times.

18

While the typical EME receiving higher capital inflows will grow 0.3

12

Gopinath, G and Stein, JC (2018), ‘Banking, Trade, and the Making of a Dominant Currency’, Working paper, Harvard University. The

euro is in second place at 20% and the yen is in third at 4% (ECB Staff (2017)).

13

Gourinchas, P, Rey, H Sauzet, M (2019), ‘The International Monetary and Financial System’, NBER Working Paper No. 25782.

14

Ilzetzki, E, Reinhart, C and Rogoff, K (2017), ‘Exchange arrangements entering the 21

st

Century: Which anchor will hold?’,

forthcoming in the Quarterly Journal of Economics.

15

See Krugman (1980).

16

Rey, H. (2013). "Dilemma not trilemma: the global cycle and monetary policy independence," Proceedings - Economic Policy

Symposium - Jackson Hole, Federal Reserve Bank of Kansas City.

17

Reflecting the fact that most of the assets of EME companies are priced in local currency. See Bruno, V and Shin, HS (2015), ‘Cross-

Border Banking and Global Liquidity’, Review of Economic Studies, Oxford University Press, Vol. 82(2), pp. 535-564 and Cesa-Bianchi,

Ferrero, Rebucci (2018), ‘International Credit Supply Shocks’, Journal of International Economics, Vol. 112, 2018, pp. 219- 237.

18

Ghosh, AR, Ostry, JD, and Qureshi, M (2016), ‘When do capital inflows surges end in tears?’, American Economic Review. Surges

are defined as a net capital flow observation that lie in the top thirtieth percentile of both the country-specific and the full sample’s

distribution of net capital flows, expressed in percent of GDP.

All speeches are available online at www.bankofengland.co.uk/news/speeches

8

8

percentage points faster, all else equal, the typical EME with higher capital flow volatility will grow 0.7

percentage points slower.

19

Following their experience of successive crises, EMEs have responded to these pressures by following the

conventional wisdom to “keep their houses in order.” Over the past two decades, inflation targeting has been

widely adopted, fiscal policy is generally improved, and macroprudential policy is increasingly active.

Bank analysis finds that, for EMEs as a whole, reforms to these domestic institutional “pull” factors have

substantially increased the sustainability of capital flows, all else equal (Chart 5).

20

But unfortunately for EMEs, all else is not equal. Their efforts have not been sufficient because of the

consequences of the growing asymmetry between the importance of the US dollar in the global financial

system and the increasingly multi-polar nature of global economic activity.

Monetary policy and financial stability shocks in advanced economies have become more prevalent and

more potent, increasing the importance of “push” factors in driving capital flows. Bank research suggests

that the spillover from tightening in US monetary policy to foreign GDP is now twice its 1990-2004 average,

despite the US’s rapidly declining share of global GDP.

Financial instability in advanced economies also causes capital to retrench from EMEs to ‘safe havens’, as it

did during the 2008 financial crisis and the 2011 euro-area crisis (Chart 6). Connally’s dictum “our dollar,

your problem” has broadened to “any of our problems is your problem”.

Moreover, the structure of the global financial system – or the “pipes” – is increasingly amplifying capital

outflows from EMEs when these push shocks occur. For EMEs, market-based finance has accounted for all

the increase in foreign lending since the crisis, as bank lending has declined and FDI has stayed fairly

constant (Chart 7).

21

While this shift has brought welcome diversity to the financial system, it also reduces

the sustainability of capital flows, as market-based flows are particularly sensitive to changes in global risk

appetite and financial conditions. Investment fund flows are particularly flighty (Chart 8), especially under

stress.

The increasing role of “push” factors and the “pipes” of the system means fast-reforming EMEs could soon

be running to stand still in their quest for more sustainable capital flows (Chart 9). Bank researchers

estimate that the growing shares of FX-denominated debt and market-based finance have increased the

sensitivity of “Capital Flows-at-Risk” to push factors by 50% since the crisis, largely using up the self-

insurance purchased by EMEs.

All told, this means that in the face of foreign shocks, EMEs are forced to compromise their monetary

sovereignty, temporarily diverting monetary policy away from targeting domestic output and inflation and

instead using it to try to stabilise capital flows.

While this strategy is the best EMEs can do given the current structure of the international monetary financial

system, outcomes for them are a distant second best when compared to those advanced economies that are

less exposed to international financial spillovers.

19

See ‘Pull, Push. Pipes’, speech by Mark Carney, Institute of International Finance Spring Membership Meeting, Tokyo, 6 June 2019.

20

Within the Bank’s Capital Flows-at-Risk framework, these actions are estimated to have Capital Flows-at-Risk (that is, capital outflows

as a percent of GDP in the fifth percentile of the distribution) by 3% of GDP.

21

Within this, investment funds are growing, accounting for the bulk of the growth in asset management over the last decade. In

parallel, investment fund flows to EMEs now account for around one third of total portfolio flows, compared to around one tenth pre-

crisis.

All speeches are available online at www.bankofengland.co.uk/news/speeches

9

9

-------------------------------

The deficiencies of the IMFS affect EMEs more directly than advanced economies, but their consequences

influence everyone because they reduce the global equilibrium interest rate.

Against the current backdrop of an inadequate and fragmented global financial safety net, EMEs have

chosen to self-insure against capital flow volatility by accumulating reserves of safe assets, contributing to

Ben Bernanke’s “global savings glut”. Given the importance of the US dollar in trade, debt issuance by the

non-financial corporate sector in EMEs, and funding for their domestic banks, most of these reserves are

dollar-denominated.

As well as coming at a domestic high cost to EMEs,

22

this vast accumulation of safe assets has pushed

down the global equilibrium interest rate – the rate that central banks must deliver in order to balance

demand with supply and so achieve stable inflation.

23

More fundamentally, by making the world a riskier place, the flaws inherent in the IMFS are reinforcing the

downward pressure on global r*.

The IMFS is not only making it harder to achieve price and financial stability but it is also encouraging

protectionist and populist policies which are exacerbating the situation. This combination reduces the rate of

global potential growth, increases its downside skew, and bolsters the likelihood of an extreme downside

event (a fatter left tail).

As my colleague on the MPC Jan Vlieghe has illustrated, such a change in the distribution of economic

outcomes reduces the global equilibrium rate of interest.

24

Past instances of very low rates have tended to

coincide with high risk events such as wars, financial crises, and breaks in the monetary regime.

Whether the last happens is still within our control, but for now the lower global equilibrium interest rate is

reducing monetary policy makers’ scope to cut policy rates in response to adverse shocks to demand, and

increasing the risk of a global liquidity trap.

And left unattended, these vulnerabilities are only likely to intensify.

25

III. Policy Implications

How should monetary policy makers respond to these challenges?

In the short term, they must play the hand they’ve been dealt.

The prevalence of dollar invoicing means using the flexibility in inflation targeting.

22

In addition to the direct costs of financing these reserves, there have been indirect costs including the crowding out of domestic

investment.

23

Rachel, L and Smith, T (2015), ‘Secular drivers of the global real interest rate’, Bank of England Staff Working Paper No. 571,

estimate that the savings glut has lowered global real rates by 25 basis points over the past 30 years.

24

See ‘Real interest rates and risk’, speech by Gertjan Vlieghe given at the Society of Business Economists’ Annual conference, 15

September 2017.

25

If history serves as a guide, EMEs’ external liabilities could double as a share of GDP by 2030: market-based finance could then

account for half of external liabilities and investment funds could represent 40% of market-based finance flows to EMEs. By 2030, the

reduction in sustainable capital flows arising from push factors could completely cancel out the positive impact stemming from domestic

reforms in EMEs over the past two decades. To offset this reduction in the sustainability of EME capital flows, their reserves would

have to double over the next ten years. [This is made more challenging by the increasing weight of EMEs in the global economy, and

the declining share of the US, which means demand for US-denominated safe assets is likely rise faster than their supply.]

All speeches are available online at www.bankofengland.co.uk/news/speeches

10

10

In theory, the increases in both DCP and capital flows at risk suggest a greater focus on targeting the

bilateral exchange rate against the dollar (through adding terms involving terms of trade misalignments and

deviations from the law of one price to central banks’ monetary policy objective functions, and tools such as

capital flow management measures (“CFM”)).

26

In practice, either could be highly destabilising. It is far better as a first response to focus on core price

stability objectives, and to explain transparently if foreign shocks are altering the trade-off required to best

achieve it.

Monetary policy makers’ mandates are necessarily parsimonious, focusing on a small set of macroeconomic

variables – price stability and maintaining output around potential. While some shocks drive inflation and

output in the same direction, others push inflation away from target without proportional effects on activity,

confronting monetary policymakers with a trade-off between these two objectives. Fluctuations in the

exchange rate can be an important source of such trade-offs, as they can exert pressures on consumer price

inflation without proportional effects on activity.

27

A simple way to represent formally how the policymaker optimises the trade-off is in “linear-quadratic” form –

a set of linear constraints describing the behaviour of the economy, and quadratic preferences that penalise

deviations of inflation from its target and output from its potential. The relative weight the policymaker places

on output stabilisation, relative to inflation stabilisation, is often denoted ߣ – or ‘lambda’.

A lambda of zero would imply no weight on the stabilisation of real activity – so-called “inflation nutter”

preferences. A positive lambda implies a willingness to strike at least some trade-off between output and

inflation stabilisation; a higher value indicates that relatively more weight is given to output stabilisation, so

that more of the effects of any shock flows through to inflation.

In this framework, the value of lambda should vary over time in light of the nature and persistence of the

shocks hitting the economy and features of the economy. The MPC’s remit explicitly builds in such flexibility.

It recognises that in exceptional circumstances, when shocks to the economy may be particularly large,

persistent or both, the MPC is likely to be faced with more significant trade-offs. In these circumstances, the

Committee can extend the horizon over which it returns inflation to target if doing so achieves a better

balance between the scale and duration of the deviation of inflation from target and the variability of output.

This same framework can be used to think through the implications of the dominance of the US dollar in

international trade and invoicing. In particular, in a DCP world with sticky dollar prices, a depreciation driven

by strength in the dollar will tend to result in additional imported inflation. Rather than tightening monetary

policy to offset fully that exogenous increase in imported inflation through lower domestic inflationary

pressures, policymakers would do better to trade off inflation and output volatility, accepting some increase in

imported inflation to achieve a smaller reduction in domestic demand below potential. The ability of new

exporters to benefit from the depreciation by undercutting existing dollar contracts would provide some boost

to exports and help lessen the trade-off facing the monetary policy maker.

A similar strategy could be pursued in the face of large financial spillovers. The ability to do this depends

heavily on the credibility of the monetary policy framework and the transparency with which the strategy is

pursued. As I will go on to discuss, both can be reinforced by explicit recognition of the spillovers of the

IMFS, particularly if recognised in IMF surveillance.

26

On the implications of DCP for optimal monetary policy, see Egorov, Konstantin and Dmitry Mukhin, “Optimal Monetary Policy under

Dollar Pricing,” March 2019. mimeo Yale University; and Casas, C, Diez, FJ, Gopinath, G and Gourinchas, PO (2017), ‘Dominant

Currency Paradigm: A New Model for Small Open Economies’, IMF Working Papers 17/264.

27

For more detail, see ‘Lambda’, speech by Mark Carney, 16 January 2017.

All speeches are available online at www.bankofengland.co.uk/news/speeches

11

11

The growing risk of a global liquidity trap puts a high premium on getting more than just monetary policy

right. Limited space for monetary policy to respond to adverse shocks means more of the burden for

supporting jobs and activity will fall to fiscal policy. Though some may be tempted to resort to protectionism,

such policies would merely serve to make the problem worse.

Those at the core of the IMFS need to incorporate spillovers and spill backs, as the Fed has been doing.

More broadly, central banks need to develop a better shared understanding of the scale of global risks and a

recognition that concerted, cooperative action may sometimes be necessary.

That doesn’t mean that monetary policy makers in advanced economies must internalise fully spillovers from

their actions on emerging market economies, given their mandates are to achieve domestic objectives. They

must, however, increasingly take account of effects that spill back on their economy as well as shifts in the

global equilibrium interest rate that their actions can spur.

28

As the weight of EMEs in the global economy has steadily risen, the size of the spillbacks from a tightening

in US financial conditions has tripled relative to its 1990 - 2004 average. With EMEs projected to account for

three quarters of the global economy by 2030, these spillbacks will only continue to grow (Chart 10).

IV. Medium term: reshuffling the deck by reforming the existing system

In the new world order, a reliance on keeping one’s house in order is no longer sufficient. The

neighbourhood too must change.

There can be innocent bystanders but there should be no disinterested observers. We are all responsible for

fixing the fault lines in the system.

Addressing Pull Factors in EMEs

EMEs can increase sustainable capital flows by addressing “pull” factors including:

- reinforcing monetary policy credibility including safeguarding the operational independence of central

banks;

- building the resilience of their banks;

- deepening their domestic capital markets to reduce the reliance on foreign currency debt; and

- expanding the scope and application of their macroprudential toolkits to guard against excessive

credit growth during booms. Bank of England research finds that tightening prudential policy in

EMEs dampens the spillover from US monetary policy by around a quarter.

29

Moderating Push Factors and Fixing the Pipes in Advanced Economies

At the same time, it is in the interests of advanced economies to moderate push factors, including risks in

their markets and institutions. Their local financial stability are global public goods.

28

For example, as Chair Powell noted in his speech ‘Monetary Policy in the Post-Crisis Era’ (July 2019), “since the crisis policymakers

are even more keenly aware of the relevance of global factors to our policies. The global nature of the financial crisis and the channels

through which it spread sharply highlight the interconnectedness of our economic, financial, and policy environments. U.S. economic

developments affect the rest of the world, and the reverse is also true.” The Federal Reserve’s recent Conference on Monetary Policy

Strategy, Tools and Communications Practices devoted a session to the global dimension of US monetary policy.

29

Coman, A, and Lloyd, S (forthcoming), ‘In the Face of Spillovers: Prudential Policies in Emerging Economies’.

All speeches are available online at www.bankofengland.co.uk/news/speeches

12

12

Consider a modern example of the Connally dictum: investment fund flows to EMEs. These flows now

account for around one third of total portfolio flows to EMEs, compared to around one tenth pre-crisis. $30

trillion of global assets are held in investment funds that are particularly flighty, reflecting their promise of

daily liquidity to investors despite investing in potentially illiquid underlying assets, such as EME debt.

30

This structural mismatch means that these funds can behave particularly pro-cyclically. Bank of England

work finds that redemptions by EME bond funds (with large structural mismatches) in response to price falls

are five times those for EME equity funds (with lower structural mismatch). In turn, EME equity funds are

twice as responsive as advanced economy equity funds.

Under stress, investment funds may need to fire sell assets, magnifying market adjustments and triggering

further redemptions – a vicious feedback loop that can ultimately disrupt market functioning and the

availability of finance to the real economy.

The vast majority of these funds are managed out of the US and Europe, including the UK. As is the case

for banks, it is a global public good to ensure that investment funds prudently manage their leverage and

liquidity.

The Bank of England is acutely conscious of these responsibilities, given the City’s role as the world’s

leading international financial centre. That’s one reason why we have transformed the resiliency of UK-

based banks, why we are well on the path to ending too big to fail, and why we have fundamentally

overhauled our liquidity facilities to support continuously open markets.

And it’s why the Bank of England’s Financial Policy Committee has supported the FSB’s 2017

recommendation that funds’ assets and investment strategies should be consistent with their redemption

terms. The Bank is now working with the FCA to assess how funds’ redemption terms, including pricing and

notice periods, might be better aligned with the liquidity of their assets in order to minimise financial stability

risks.

31

More effective and impactful IMF surveillance

The deficiencies in the current IMFS mean that the IMF should play a central role in informing both domestic

and cross border policies. In particular, discussions at the Fund can identify those circumstances when

spillovers from the core are particularly acute. This in turn can help guide central banks’ use of the flexibility

inherent in their monetary policy frameworks, the deployment of macroprudential tools and, in extremis,

capital flow management measures.

32

In these regards, transparent, evidence-based discussions convened

by the IMF can both discipline policy and avoid potentially antagonistic misunderstandings that could lead to

de-stabilising tit-for-tat retaliations.

Reinforcing the GFSN

The IMF’s core liquidity function can also play a more important role. Collective action should improve the

adequacy of the global financial safety net (GFSN) to reduce the need for EMEs to accumulate reserves of

safe assets as insurance against less sustainable capital flows. Over the past two decades, the GFSN has

30

Estimates are based on the FSB’s measure of ‘collective investment vehicles with features that make them susceptible to runs’; see

FSB Global Monitoring Report on Non-Bank Financial Intermediation 2018.

31

The review will also assess the effectiveness of measures that are already used to deal with misalignment of redemption terms and

asset liquidity, such as swing and fair value pricing and suspensions.

32

For example, limits on foreign currency borrowing and restrictions on the activities of open-ended investment funds. History has

shown that capital flow management measures can be both addictive and highly distortionary. That is why the IMF’s Institutional View

makes clear that CFM should not substitute for domestic institutional reforms or warranted macroeconomic adjustments.

All speeches are available online at www.bankofengland.co.uk/news/speeches

13

13

become more fragmented and its core – IMF resources – has shrunk relative to the size of the global

financial system (Chart 11).

Pooling resources at the IMF, and thereby distributing the costs across all 189 member countries, is much

more efficient than individual countries self-insuring. To maintain reserve adequacy in the face of future

larger and more risky external balance sheets, EMEs would need to double their current level of reserves

over the next 10 years – an increase of $9 trillion. A better alternative would be to hold $3 trillion in pooled

resources, achieving the same level of insurance for a much lower cost. This would imply a tripling in the

IMF’s resources over the next decade, enough to maintain their current share of global external liabilities.

33

One of the many advantages of this approach is it would reduce the demand for safe assets and with it, the

downward pressure on r*.

V. Long term: Changing the Game

While such concerted efforts can improve the functioning of the current system, ultimately a multi-polar

global economy requires a new IMFS to realise its full potential.

That won’t be easy.

Transitions between global reserve currencies are rare events given the strong complementarities between

the international functions of money, which serve to reinforce the position of the dominant currency.

And the most likely candidate for true reserve currency status, the Renminbi (RMB), has a long way to go

before it is ready to assume the mantle.

The initial building blocks are there. Already, China is the world’s leading trading nation, overtaking the US

at the start of this decade.

34

And the Renminbi is now more common than sterling in oil future benchmarks,

despite having no share in the market prior to 2018.

35

The greater use of the Renminbi in international trade is also leading to its growing use in international

finance. This has been enabled by reforms to China’s monetary, foreign exchange, and financial systems

that have liberalised and improve its financial market infrastructure, making the Renminbi a more reliable

store of value.

36

The Belt and Road Initiative could foster further take up of the Renminbi in both trade and

finance.

However, for the Renminbi to become a truly global currency, much more is required. Moreover, history

teaches that the transition to a new global reserve currency may not proceed smoothly.

Consider the rare example of the shift from sterling to the dollar in the early 20

th

Century – a shift prompted

by changes in trade and reinforced by developments in finance.

37

The disruption wrought by the First World

War allowed the US to expand its presence in markets previously dominated by European producers. Trade

33

The design of the GFSN is also important. Positive steps have been made in recent years by introducing precautionary liquidity

facilities so countries can borrow to prevent crises, as well as mitigate their impact. This should also reduce stigma of drawing on the

facilities. But so far, only a few countries have taken them up. It is important to do everything we can to normalise use of these

precautionary facilities.

34

World Bank.

35

Taken from The International Role of the Euro June 2019, ECB.

36

Initiatives include trade settlement programs, RMB offshore clearing banks, off-shore RMB denominated bond market in Hong Kong,

and a network of central bank RMB swap lines.

37

For more details, see Eichengreen, B J (2008), ‘Globalizing capital: A history of the international monetary system’, Princeton:

Princeton University Press; and Eichengreen, B, Mehl, A, and Chiţu, L (2018), ‘How Global Currencies Work: Past, Present, and

Future’, Princeton University Press.

All speeches are available online at www.bankofengland.co.uk/news/speeches

14

14

that was priced in sterling switched to being priced in dollars; and demand for dollar-denominated assets

followed. In addition, the US became a net creditor, lending to other countries in dollar-denominated bonds.

Institutional change supported the role of the dollar, with the creation of the Federal Reserve System

providing, for the first time, a market-maker and liquidity manager in US dollar acceptances. This was

particularly helpful for promoting the use of the dollar in trade credit, reinforcing its use as a means of

payment and invoicing currency.

Yet the US was, at least at first, an unwilling hegemon. Under the gold standard, the Fed’s absorption of

gold inflows exported significant deflationary pressures to the rest of the world.

38

Europe was dependent on

the recycling of capital flows by the US, which lent much of its surplus back to Europe to enable payments of

war reparations and debt. Europe suffered severely when this stopped in 1928. Moreover, the increase in

price levels that occurred as a result of the First World War left the global economy with too little gold in total

to sustain money supply at the level consistent with full employment. Supplementing gold reserves with

foreign exchange to boost money supply led to competition between the UK and the US to provide that

service to other countries.

The resulting world with two competing providers of reserve currencies served to destabilise the international

monetary system, and, some would argue, the lack of coordination between monetary policy makers during

this time contributed to the global scarcity in liquidity and worsened the severity of the Great Depression.

39

The experience of the interwar period is a cautionary tale.

When it comes to the supply of reserve currencies, coordination problems are larger when there are fewer

issuers than when there is either a monopoly or many issuers. While the rise of the Renminbi may over time

provide a second best solution to the current problems with the IMFS, first best would be to build a multipolar

system.

The main advantage of a multipolar IMFS is diversification. Multiple reserve currencies would increase the

supply of safe assets, alleviating the downward pressures on the global equilibrium interest rate that an

asymmetric system can exert. And with many countries issuing global safe assets in competition with each

other, the safety premium they receive should fall.

40

A more diversified IMFS would also reduce spillovers from the core and by so doing lower the

synchronisation of trade and financial cycles. That would in turn reduce the fragilities in the system, and

increase the sustainability of capital flows, pushing up the equilibrium interest rate.

While the likelihood of a multipolar IMFS might seem distant at present, technological developments provide

the potential for such a world to emerge. Such a platform would be based on the virtual rather than the

physical.

38

For a comparison with the UK as a hegemon in the period 1870-1914, see van Hombeeck, C (2017), ‘An exorbitant privilege in the

first age of international financial integration’, Bank of England Staff Working Paper No. 668.

39

Investors switched between pound and dollar depending on their perception of each country, leading to increased volatility in currency

flows. Countries were forced to raise policy rates in an attempt to attract scarce gold reserves, dampening domestic spending – a

position that ultimately proved unsustainable. These coordination problems led to lower issuance of safe assets in total and meant the

potential benefits from competition between alternative providers of reserve currencies were not realised. In retrospect, a more

cooperative solution would have allowed countries to cut policy rates in a coordinated manner, providing support to domestic demand

without affecting pressures on gold flows.

40

Farhi, E, and Maggiori, M (2018), ‘A Model of the International Monetary System’, Quarterly Journal of Economics 133 (1): 295-355.

All speeches are available online at www.bankofengland.co.uk/news/speeches

15

15

History shows that the rise of a reserve currency is founded on its usefulness as a medium of exchange, by

reducing the cost and increasing the convenience of international payments. The additional functions of

money – as a unit of account and store of wealth – come later, and reinforce the payments motive.

Technology has the potential to disrupt the network externalities that prevent the incumbent global reserve

currency from being displaced.

Retail transactions are taking place increasingly online rather than on the high street, and through electronic

payments over cash. And the relatively high costs of domestic and cross border electronic payments are

encouraging innovation, with new entrants applying new technologies to offer lower cost, more convenient

retail payment services.

The most high profile of these has been Libra – a new payments infrastructure based on an international

stablecoin fully backed by reserve assets in a basket of currencies including the US dollar, the euro, and

sterling. It could be exchanged between users on messaging platforms and with participating retailers.

41

There are a host of fundamental issues that Libra must address, ranging from privacy to AML/CFT and

operational resilience. In addition, depending on its design, it could have substantial implications for both

monetary and financial stability.

42

The Bank of England and other regulators have been clear that unlike in social media, for which standards

and regulations are only now being developed after the technologies have been adopted by billions of users,

the terms of engagement for any new systemic private payments system must be in force well in advance of

any launch.

As a consequence, it is an open question whether such a new Synthetic Hegemonic Currency (SHC) would

be best provided by the public sector, perhaps through a network of central bank digital currencies.

Even if the initial variants of the idea prove wanting, the concept is intriguing. It is worth considering how an

SHC in the IMFS could support better global outcomes, given the scale of the challenges of the current IMFS

and the risks in transition to a new hegemonic reserve currency like the Renminbi.

An SHC could dampen the domineering influence of the US dollar on global trade. If the share of trade

invoiced in SHC were to rise, shocks in the US would have less potent spillovers through exchange rates,

and trade would become less synchronised across countries.

43

By the same token, global trade would

become more sensitive to changes in conditions in the countries of the other currencies in the basket

backing the SHC.

The dollar’s influence on global financial conditions could similarly decline if a financial architecture

developed around the new SHC and it displaced the dollar’s dominance in credit markets. By reducing the

influence of the US on the global financial cycle, this would help reduce the volatility of capital flows to EMEs.

Widespread use of the SHC in international trade and finance would imply that the currencies that compose

its basket could gradually be seen as reliable reserve assets, encouraging EMEs to diversify their holdings of

safe assets away from the dollar. This would lessen the downward pressure on equilibrium interest rates

and help alleviate the global liquidity trap.

41

See https://libra.org/en-US/.

42

For more details, see ‘Enable, Empower, Ensure: A New Finance for the New Economy’, speech by Mark Carney, at the Lord

Mayor’s Banquet for Bankers and Merchants of the City of London at the Mansion House, London, 20 June 2019.

43

This requires that the other currencies included in the basket backing the global currency are not perfectly correlated with the dollar,

which seems likely to be the case given countries face idiosyncratic shocks.

All speeches are available online at www.bankofengland.co.uk/news/speeches

16

16

Of course, there would be many execution challenges, not least the risk of fragmentation across Digital

Currency Areas.

44

But by leveraging the medium of exchange role of a reserve currency, an SHC might

smooth the transition that the IMFS needs.

Conclusion

20 years ago, the theme of this symposium was “New Challenges for Monetary Policy”, and my predecessor,

Mervyn King, was one of the speakers. His reflections were on the merits of inflation targeting and flexible

exchange rates. The applications of his insights have contributed greatly to improved economic outcomes

around in the world in the intervening years.

But during that same period, the deficiencies of the IMFS have become increasingly potent. Even a passing

acquaintance with monetary history suggests that this centre won’t hold. We need to recognise the short,

medium and long term challenges this system creates for the institutional frameworks and conduct of

monetary policy across the world. Given the experience of the past five years, I will close by adding urgency

to Ben Bernanke’s challenge. Let’s end the malign neglect of the IMFS and build a system worthy of the

diverse, multipolar global economy that is emerging.

44

For more discussion of this, see Brunnermeier, MK, James, H and Landau, JP (2019), ‘Digital currency areas’, VoxEU.

All speeches are available online at www.bankofengland.co.uk/news/speeches

17

17

Annex

I. Challenges for Monetary Policy in the current IMFS

Figure 1: The US dollar continues to be as important today as it was during the Bretton Woods era

Chart 1: Trade war is the top tail risk affecting global investors

Sources: Bank of America Merrill Lynch Global Fund Manager Survey.

0 102030405060

Brexit

European elections

Equity market bubble

Market structure

US politics

Populist policies

Iran

A credit event

Bond market bubble

China slowdown

Monetary policy impotence

Trade war

July 2019

June 2019

March 2019

Percentage of respondents

All speeches are available online at www.bankofengland.co.uk/news/speeches

18

18

Chart 2: Global economic policy uncertainty has reached record highs

Source: Baker, S, Bloom, N and Davis, S (2015), ‘Measuring economic policy uncertainty’, NBER Working Paper

No. 21633.

II. Growing challenges in the Current IMFS

Chart 3: Volatile capital flows amplify domestic imbalances in EMEs

Net private capital flows to emerging market economies and incidences of crises

Source: IMF.

Notes: Excludes China

USS Cole

bombings

9/11

Iraq

invasion

Madrid

bombings

London

bombings

Transatlantic

aircraft plot

Ukraine / ISIS

Paris attacks

US implements first

China-specific tariffs

25

50

75

100

125

150

175

200

225

250

275

300

325

350

375

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Index

-1

0

1

2

3

4

5

6

0

1

2

3

4

5

6

1980 1985 1990 1995 2000 2005 2010 2015

Number

% of GDP

Number of EM crises (rhs)

Net private capital flows to Non-China EMEs (lhs)

Crises tend to occur

when capital flows slow

All speeches are available online at www.bankofengland.co.uk/news/speeches

19

19

Chart 4: Greater reliance on foreign investors increases capital flow volatility

Correlation of capital flow volatility and the share of FX-denominated corporate debt

Sources: IMF and IIF.

Notes: Measured as coefficient of variation of gross inflows scaled by external liabilities.

Chart 5: Pull factors have reduced Capital Flows at-risk for EMEs since the Asian Financial Crisis

Sources: IMF and Bank staff calcluations.

Notes: Chart shows the contribution of pull factors to capital flows to EMEs during the Asian Financial Crisis (purple),

and since 2008 (green). The diamonds highlight the fifth percentile, which is our preferred measure of Capital Flows-

at-Risk. In both distributions push factors are held at their sample average, so only pull factors are changing.

TUR

ZAF

ARG

BRA

CHL

COL

MEX

ISR

IND

IDN

KOR

MYS

THA

RUS

CHN

CZE

POL

0.0

0.5

1.0

1.5

2.0

0 1020304050

Volatity of capital flows

Share of non-financial corporate debt denominated in USD

0.00

0.02

0.04

0.06

0.08

0.10

0.12

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18

Probabilty density

Capital flows as a % of GDP

Post-2008 crisis Asian Financial Crisis

B

A

All speeches are available online at www.bankofengland.co.uk/news/speeches

20

20

Chart 6: Push shocks have offset some of the improvements in the ‘pull factors’

Sources: IMF and Bank staff calculations.

Note: The grey bars on this chart show the unconditional 5th percentile of the distribution of capital flows in a panel of

13 EMEs since 1996. The purple bars build on the contribution of pull factors to the conditional 5th percentile of

capital flows in the current quarter and two quarters ahead. Pull factors are proxied by domestic financial condition

indices (DFCIs), which are mean-orthogonalised by a global financial conditions index (GFCI). The coefficient on the

DFCIs is estimated by panel quantile regressions. Push factors are proxied by the Bank of England’s global financial

conditions index. The chart shows PPP-weighted averages across the 13 EMEs in our panel.

Chart 7: For EMEs, market-based finance accounted for all the increase in foreign lending since the

crisis

Structure of external liabilities for emerging market economies

Sources: IMF, EPFR and Bank of England calculations

‐8

‐6

‐4

‐2

0

2

1996 1999 2002 2005 2008 2011 2014 2017

AverageCapitalFlows‐at‐Risk

Contributionofpullfactors

Contributionofpushfactors

TotalCapitalFlows‐at‐Risk

Gross

outflow

Gross

inflows

Capital Flows as a % of GDP

All speeches are available online at www.bankofengland.co.uk/news/speeches

21

21

Chart 8: Market-based finance flows are particularly sensitive to push shocks

The sensitivity of Capital Flow-at-Risk to push factors, by source of capital flow

Sources: IMF, EPFR, Bank calculations.

Notes: Chart shows the sensitivity of different capital flows to a negative "push" shock. Coefficients are standardised

by each component’s share of total flows e.g. the red MBF bar shows how total Capital Flows-at-Risk would

respond to a one standard deviation tightening in global financial conditions if all capital flows were accounted for by

MBF.

Chart 9: Emerging market economies could be running to stand still in the future

Sources: IMF, EPFR, IIF and Bank staff calculations.

Notes: This chart shows conditional distributions of capital flows to EMEs post-the 2008 crisis (green), and

conditioning on a one standard deviation negative “push shock” (red), as proxied by our global financial conditions

index. The diamonds highlight the fifth percentile, which is our preferred measure of Capital Flows-at-Risk The dotted

grey distribution results from increasing the sensitivity of the distribution to push shocks in line with the scalar in the

third column of chart 10, assuming they apply through the distribution (rather than only to 5th percentile). Estimating

the impact of these vulnerabilities on the full distribution is a rich area for future work. The teal distribution conditions

on average push and pull factors 1996-06.

-5

-4

-3

-2

-1

0

FDI Banking Market-based finance

of which: investment

funds

Median 5th percentile

Capital Flows-at-Risk as a % of GDP

0.00

0.02

0.04

0.06

0.08

0.10

0.12

‐8‐6‐4‐2024681012141618

Probabilitydensity

Capitalflowsasa%ofGDP

Average2009‐18

Average1996‐06

Impactofpushfactors

Impactofpushfactorswith2030amplificationduetoshiftingcomposition(col3,chart10)

All speeches are available online at www.bankofengland.co.uk/news/speeches

22

22

Chart 10: Major structural changes are increasing the sensitivity of Capital Flows-at-Risk to push

shocks

Sources: IMF, EPFR, IIF, Bank calculations.

Notes: This chart shows estimates and projections for the sensitivity of Capital Flows-at-Risk to negative push shocks

at different points in time. The chart is based on separate panel quantile regressions for FDI, banking, market-based

finance and investment fund flows. We use the global FCI (push), country-specific FCIs (pull), and the share of NFC

debt denominated in foreign currency as regressors. The third bar combines regression results with projections for

the composition of flows and the role of FX-denominated debt in 2030. The fourth bar also takes into account

projected growth in EM’s external balance sheets.

IV. Medium term: reshuffling the deck by reforming the existing system

Chart 11: IMF resources, the core of global financial safety net, has shrunk relative to the size of the

global financial system

Components of the global financial safety net as a per cent of global external liabilities

Sources: IMF, central bank websites, Lane Milessi-Ferretti (2007) External Wealth of Nations dataset and Bank

calculations.

Notes: FX reserves exclude gold.

-4

-3

-2

-1

2006 2018

2030 excluding growth

in EME external balance

sheets

2030 including growth in

EME external balance

sheets

Capital Flows-at-Risk as a % of GDP

Impact of the increasing role of investment funds

Impact of the shift to market-based finance

Impact of higher share of FX-denominated debt in EMs

Pre-crisis

Total

0

2

4

6

8

10

12

0

1

2

3

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

IMFPermanent(rhs) IMFTemporary(rhs)

FXReserves(lhs)

Per cent of global

external liabilities

Per cent of global

external liabilities

All speeches are available online at www.bankofengland.co.uk/news/speeches

23

23

Chart 12a: UK monetary policy trade-offs in successive 2-year ahead Inflation Report projections

Chart 12b: UK monetary policy trade-offs in successive 3-year ahead Inflation Report projections

Notes to Chart 12: Each observation shows the central projection for spare capacity or excess demand at the end of the

second / third year of the forecast period (the 'Year 2' or ‘Year 3’ point) on the horizontal axis against the central

projection for four-quarter CPI inflation at Year 2 / Year 3 on the vertical axis from successive Inflation Reports. See

’Lambda’, speech by Mark Carney, 16 January 2017, for further details and discussion.

1.0

1.5

2.0

2.5

3.0

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Inflation (%)

Excess

Preferred trade-off if λ=1

Preferred trade-off

if λ=0.1

Excess

supply

(%)

August

2016

August 2019

1.0

1.5

2.0

2.5

3.0

-1.0 -0.5 0.0 0.5 1.0 1.5 2.0

Inflation (%)

Excess

Preferred trade-off if λ=1

Preferred trade-off

if λ=0.1

Excess

supply

(%)

August

2016

August 2019