TRANSACTIONS OF SOCIETY OF ACTUARIES

1980 VOL. 32

PRICING A SELECT AND ULTIMATE ANNUAL

RENEWABLE TERM PRODUCT

JEFFERY DUKES AND ANDREW M. MACDONALD

ABSTRACT

This paper discusses the special considerations involved in pricing a

select/ultimate annual renewable term product. It covers such areas as

expenses, conversion costs, and profit calculation, and devotes particular

attention to the relationship between mortality and withdrawals on this

type of product. A general equation for computing the extra mortality

under various lapse assumptions is developed.

INTRODUCTION

H

IGH interest rates in recent years have led increasingly to a

"buy term and invest the difference" strategy among insureds.

Insurance companies, like all competitive businesses, must

shape their products to fit the desires of their market. This need, com-

bined with the increasing emphasis on term insurance, has intensified

competition for the term insurance sale. Many companies hope that their

term sales will result in conversions to permanent plans, but some view

the term market as a profitable end in itself. In this market there is no

competition keener than that for annual renewable term (ART)--or

yearly renewable term (YRT). A few years ago, some of the innovative

smaller companies began marketing a select and ultimate ART (S/U

ART) product. Having just completed the pricing of such a product,

which, we believe, could well become the top term product in most port-

folios, we felt it might be helpful to discuss our methods and provoke

some discussion within the profession.

PRODUCT DESCRIPTION

The usual ART product (which we call the aggregate ART) has

annually increasing premiums that vary by attained age only. As the

name implies, S/U ART has annually increasing premiums that vary by

issue age and duration since underwriting. For the first few durations

after underwriting, premiums are quite low; these durations constitute

the select period, which generally lasts four or five years, although,

547

548 SELECT AND ULTIMATE RENEWABLE TERM

beginning in late 1979, products with a one-year select period began

appearing on the market, and products with select periods of ten or

fifteen years are not unheard of. While the logical select period would

seem to be the select period inherent in the mortality table used for

product pricing, in practice one sees the range mentioned above.

At the end of the select period, the insured will pay premiums from the

ultimate rate scale; these premiums vary only by attained age. The

insured can seek to avoid paying these higher ultimate rates by exercising

the reversion feature usually found in S/U ART plans. This feature

gives the insured the opportunity at the end of the select period (or

earlier for some of the products with long select periods) to provide new

evidence of insurability at the company's expense; if the insured is still

a standard risk, a new policy is issued at the select rate for the new

issue age. The annually revertible (one-year select period) products of

which we are aware have less stringent requirements for reversion. The

insured may only have to answer three or four questions about his

health in the past year. Presumably, much of the excess mortality over

that of a new issue is offset by reduced underwriting costs.

The reversion process can be repeated as long as the insured remains

a standard risk and below a specified age (typically 70). In the case of a

reversion, the agent usually receives a commission equal to 50-100

percent of the first-year commission for a new issue. In this paper, we

will examine S/U ART products that require full evidence of insurability

for reversion and that pay a full first-year commission to the agent

upon reversion. Table 1 compares aggregate ART and S/U ART rates

(five-year select period) for issue age 45.

PRICING ASSUMPTIONS

Mortality and Lapses

These will be treated together, since we believe they are intimately

connected and are of fundamental importance in pricing this product.

We will assume that lapse and mortality experience is available for an

aggregate ART plan and that we are attempting to produce premiums

for an S/U ART product. Any lapses in excess of the corresponding

aggregate ART lapses will be called "reversions." Insureds who do not

revert will be called "persisters." We will start with two examples,

which we will then expand into a generalized formula for computing

mortality rates.

Suppose, for the first example, that we have a select and ultimate

ART product with a five-year select period. In pricing the product, we

assume that lapses in years 1-4 and in years 6 and over are the same as

SELECT

AND ULTIMATE

RENEWABLE TERM

549

those for aggregate ART (that is, no reversions occur in those years);

however, to consider the reversion feature, we assume that there is a

single reversion of 50 percent of the survivors at the end of year 5 and

that these "reverters" are all standard risks. (These "lapses" due to

reversion at the end of year 5 are assumed to be in addition to the normal

lapses that might be experienced on an aggregate ART where there is

less incentive to lapse to obtain a lower premium.) It should be noted

that this is not a realistic assumption, since insureds could revert and

obtain a lower premium before the end of the select period either with

another company or with the same company if such a practice were

allowed. Nevertheless, let us assume now, for simplicity, that the only

reversions occur at the end of the fifth year.

TABLE 1

COMPARISON OF RATES FOR S/U ART AND AGGREGATE ART

] S/U ART

J

Isstre Aoo~- ]" Select Yesrs Ultimate Years

GATE

ACZ ART

45 ..........

46 ..........

47

..........

48

..........

49 ..........

50 ..........

51 .........

52 ..........

53 ..........

54 ..........

55 ..........

56 ..........

57 ..........

58 ..........

59 ..........

60 ..........

61 ..........

62 ..........

63 ..........

64 ..........

65 ..........

66 ..........

67 ..........

68 ..........

69 ..........

70 ..........

71 ..........

72 ..........

73 ..........

74 ..........

75 ..........

76 ..........

77 ..........

78 ..........

79 ..........

1 2 3 4

4.86 2.98 4.13 5,70 6.92

5.31

5.79

6.33

6.91

7.56 3.83 5.84 8.31 10.42

8.25

9.05

9.86

10.75

11.74 5.03 7.87 12.23 16.08

12.88

14.13

15.46

16.93

18.54 7.67 11.36 18.59 25,18

20.26

22.14

24.08

26.12

28.77 13.19 18.83 29.13 38.60

31.42

34.15

37.25

40.80

45.77 21.88 29.24 43.32 [ 54.21

51.44

5793

65.23

73.28

81.37

90.46

100.59

110.75

123.90

5 Attained Rate

Age

8.15 50 9.45

51 10.31

52 11.31

53 12.33

54 13.44

12.53 55 14.68

56 16.10

57 17.66

58 19.33

59 21.16

19.96 60 23.18

61 25.33

62 27.68

63 30.10

64 32.65

31.77 65 35.96

66 39.28

67

42.69

68 46.56

69 51.00

48.06 70 57.21

71 64.30

72 72.41

73 81.54

74 91.60

74.96

75

101.71

76

113.08

77 125.74

78 138.44

79 154.88

550 SELECT AND ULTIMATE RENEWABLE TERM

Assume, then, that qf,j+t represents the aggregate ART mortality rate

and

(qP)r~+t

the mortality rate for the persisters on a select and ultimate

ART product. Because it is assumed that those who revert must meet

full standard underwriting requirements for a new issue, those who

revert at the end of policy year n will "start over" with mortality rate

(qr)tI~l+,]+~. Under our assumption of full underwriting at reversion,

(qr)t[xl+,]+t =

qtz+,l+t, where x + n is the age at reversion. In addition,

we assume that the total deaths experienced by the reverters and per-

sisters will equal the total deaths that would be experienced by a group

of the same size on an aggregate ART product. We also assume that the

underlying lapse rates (apart from the reversion rate) for reverters and

persisters are the same and are equal to those of an aggregate ART plan.

These assumptions lead to three conclusions:

1. (qP)r,~+t = qf.j+t

for t < 5. This follows from the assumption that lapse

rates are the same for both the aggregate ART and S/U ART products

before the end of the fifth year. It also assumes that there is no additional

antiselection on an S/U ART and that underwriting standards are the same

for both products.

2. (qP)tzl+t

> qt.l+t for 5 _< t < 5 + (select period in pricing mortality table).

This follows from the assumption that the 50 percent that leave the popula-

tion through reversion at the end of year 5 are all standard risks, indicating

that the persisters have a mortality rate higher than that of the comparable

aggregate class.

3. (qP)|zl+, = ql~l+t for t > 5 + (select period in pricing mortality table).

This follows from the assumption that total deaths for persisters and

reverters equal total deaths under an aggregate ART product. Thus, after

the effects of selection assumed in the pricing mortality table have worn

off, persisters and reverters experience the same mortality rates.

These conclusions will be seen more clearly in the development of

the formulas needed to calculate (qP)izl+t- To develop those formulas,

we add the following definitions to those we already have:

/t,l+t = Total number of survivors t years after issue at age x

= Total number of reverters and persisters at duration t.

(lp)i,~+t

= Number of persisters at duration t after issue at age x.

(lr)Nxj+,j+t

= Total number of survivors t years after reversion at age

x + n, where the original issue age was x. Note that a

distinction is being made between, say,

(It)H351+51+,

(which

represents total survivors t years after reversion at age

40 for issue age 35) and ll,01+, (which represents total

survivors t years after issue at age 40).

W

qt*l+* = Aggregate ART lapse rate at duration t.

SELECT AND ULTIMATE RENEWABLE TERM

dt~l+ t =

(@)~,1+,

=

(dr) u,~+.l+t =

(dr)~+.~+, =

Note that all

551

Total number of deaths between durations t and t + 1

after issue at age x

Total number of deaths among reverters and persisters

between durations t and t + 1.

ltzl+tq~=l+t.

Number of deaths among persisters between durations t

and t + 1 after issue at age x.

l ~'

( P)t~l+tq[~l+t"

Number of deaths between durations t and t + 1 after

reversion at age x + n.

l,+t functions are calculated as l~+t = l~+t_l - d,+t_x -

d~-t-1,

where dz~+t reflects expected lapses under an aggregate ART

product. Similar formulas apply to the calculation of

(lp),+,

and

(lr)~-t.

Note also that the rate of lapse, q~+t, is assumed to be the same for

persisters and reverters.

Given these assumptions and definitions, the following formulas

emerge (see Appendix I for a comparison of aggregate ART mortality

and S/U ART persister mortality as produced by these formulas).

First,

(lr)[c,l+51

= 0.5/f=j+5,

(lp)~,l+5 =

0.5/~=j+5,

Second,

qf,7+5l:~]+5 = (qp)[~]+5(lp)t=j+5

+

(qr)ff,j+5~ (lr) tE~l+~ ,

(qP)

~,~+5 = qt,l+~/t~l+5 --

(qr) tt=l+sl (lr)

tt,l+~l

(lp)~,~+~

= /t,~+~(qt,~+~ -- 0.5q[~+5~) since (qr)[f,]+~l = q[,+~]

0.5/[~1+~

= 2q~,~+.~- q[~+~].

Third,

Thus,

where

and

d[zl+e =

(dP)t~l+6 +

(dr)[t~l+~l+l.

q~zl+el[~]+8 = (qp)t~7+~(IP)~1+6

+

(qr)fm+5]+l(Ir)[r~+~l+~ ,

(lp) E,I+8 = (lp)t~1+5[1

--

(qp) ~1+5 --

qr'~J+5]

(Ir) ff~+sJ+l = (Ir)[~,l+sj

(1 -- qt[,J+sl -- q[~l+5) •

552

SELECT AND ULTIMATE RENEWABLE TERM

Thus,

(qp)~.~+, =

qt,~+*l[~'~+~ --

(qr)tt.l+~l+a(lr)tI~,~+sl+~

(lp)[.l+s[1

--

(qp)~.l+s

-- q(~l+~]

= q[~1+6l~..|+6 -- q[.~+~7+l(lr)r[.l+~l~-x

(lp)

I.~+~[ 1 --

(qp)txl+5 -- qI~l+5]

'

since

(qr)it,~+b~+~

= qt~-n~+a.

Fourth, in general, for t >_ 6,

(qP)

t.l+t =

q~.j+,lc.j+~ -- qr.+~+~_~(lr),.~+~+,_~

(~P)~+,

where

and

(lp) t~]+,

=

(lp) r.1+t_l[1

--

(qp) t.]+,_l --

qi'~l+t-al]

(lr) tt=l+51+t_5

=

(lr)[t~l+51+,_e[1

--

(qr) tt~1+51+t_6

-- q[~l+,-t] •

Fifth, for t > 5 + (pricing mortality select period),

q~x7+t = (qr)~j+51+e-5 ---- qc~+sJ+~-s = q~+~

---- Ultimate pricing mortality.

Thus,

(qP)t.l+* = q*+'[/f'J+'- (/r)fl.j+~j+,_~]

(lp)

E.I+,

Since total deaths and withdrawals for reverters and persisters under an

S/U ART product are the same as total deaths and withdrawals under

an aggregate ART product,

d[.l+, --

(dp)l~l+t + (dr)[[~l+Sl+t-5

and

which implies

or

dt'.]+t

(dP)t,]+, + ,o

= ~, (dr) [~l+51+t_~,

It.j+, = (lp)t.j+, + (lr)tfxj+sj+,_5,

(lp) cxl+, = lt.l+, --

(tr) ti.l+~l+,_5.

Thus the equation in the fifth statement above reduces to

(qp)Exi+t-~

qx+t.

Two observations are in order. First, it is not necessary to consider

further reversions among the reverters when calculating

(qP)~xl+t.

This

follows from our basic observation that the total number of deaths for

a group of policyholders is the same regardless of how the group is split--

SELECT AND ULTIMATE RENEWABLE TERM 553

a sort of conservation-of-total-deaths principle. The basic components

in the calculation of

(qP)c~l+~

are (1) deaths in the (t + 1)st policy year

from the entire group of policies issued at age x, namely,

d~+t,

and

(2) deaths among reverters, namely,

C

(~)

co.,+.,+,-. •

n=1

The conservation-of-total-deaths principle implies that deaths among

persisters in the (t + l)st policy year equals (1) - (2). The point of the

observation is that none of the terms of the sum in (2) is affected by

reversions after the reversion that gave rise to the term in the first place.

This follows from applying the conservation-of-total-deaths principle to

each group of reverters, (/r)[txl+~l+t-,, giving rise to the terms in (2). An

analogue to the conservation-of-total-deaths principle can be found in

the conservation-of-total-momentum principle of physics. Picture a

particle, T, moving along with momentum Mr. Suddenly T splits into

two particles, R (as in reverter) and P (as in persister), with momenta

MR and

MR,

respectively. Then MR + Mp - Mr. If one knows Mr and

Mm one can calculate Mp. If R splits into two or more fragments, we

know that the momenta of the fragments add up to the momentum of

R, so consideration of the fragments adds nothing but unnecessary

complication to the computation of Mp.

The second observation is that the more reverters there are, the higher

(qP)[x]+t

will be. This is intuitively obvious, since when a closed group

loses its better risks, the mortality for those remaining clearly will be

worse than that for the group before the loss.

The second observation leads to some real pricing headaches. The S/U

ART products currently on the market generally have minimum issue

amounts of at least $100,000. Consequently it seems reasonable to assume

that the insureds who purchase these products are on the whole fairly

sophisticated and likely to take advantage of situations that will decrease

their cost. In other words, one would expect reversions before the limiting

date specified in the policy form. Thus our simple assumption of 50

percent reversions at the end of year 5 with no earlier reversions is

probably unrealistic. These reversions before the end of the select period

create higher than aggregate ART mortality in the remaining select

years and decrease the number of insureds over which expenses can be

amortized, thus leading to a steeper premium scale. But the steeper the

premium scale, the greater the advantage to be obtained by applying

for a new select rate. In other words, pessimistic assumptions have a

tendency to be self-fulfilling (at least on paper--we have no experience

554 SELECT AND ULTIMATE RENEWABLE TERM

to go by). One way to combat this problem would be to offer an n-year

renewable and convertible term product such that, at the end of n years,

the product would be renewable at a relatively low rate if satisfactory

evidence of insurability were provided, but at a relatively high rate if

no evidence were furnished.

Another problem with an S/U ART product is that slightly substan-

dard cases in the ultimate years may prefer to lapse the S/U product

and purchase an aggregate ART product rather than pay ultimate

premiums. Such lapses further steepen the premium scale and ex-

acerbate the problem mentioned above of steep premiums causing higher

lapses leading to higher mortality and yet higher premiums. Let us hope

this is a convergent sequence.

If it is assumed that there will be reversions before the end of the

select period, the expected mortality rates will be affected. Suppose, as

our second example, we assume the following pattern of reversions:

1. No one reverts in policy years 1 and 2.

2. 30 percent of the survivors revert at the end of policy year 3.

3. 10 percent of the survivors revert at the end of policy year 4.

4. 20 percent of the survivors revert at the end of policy year 5.

In the authors' view, this pattern of reversions probably is more realistic,

given the mobile nature of the middle- and higher-amount term market.

We again assume that these reversions are in addition to the normal

lapses that one might expect in the case of an aggregate ART product.

We also assume that all of these reversions are standard risks.

Under this set of assumptions the following formulas would emerge

(see Appendix II for a comparison of aggregate ART mortality and S/U

ART persister mortality produced by these formulas).

First,

(lr),~+.~l

= 0.3/~,~+3,

(lp)rxj+3

= 0.71c,7+3,

where/t~]+~ is some convenient radix;

(dr) it,l+31

=

(qr)(t~]+s] (lr)frx1+31 ,

(dp) cxl+3

=

(qP) fxJ+3(lP)t~l+3,

d(~]+~ = q[~l+3lt~l+a •

Since d[~l+3

=

(dr)tt,l+a ] + (dp)[~]+~ , then

q[~l+alt~l+s =

(qr)(t~]+~l (lr)(txl+al

+

(qP)[~]+3(lP)(~+3,

(qP)(~l+~

= q[~]+31[,]+~ -- qt~+3l(lr)[~,l+al

(lp)~,~+~

because (qr)tt~]+a] = q[,+31 •

Second,

SELECT AND ULTIMATE RENEWABLE TERM 555

d W ,

(lr)[txl+41 =

O.l[(lp)txl+s- (dP)txl+s- (

p)[,l+s]

d to

(lP)t,~+4 = 0.9[(lp)t,l+z-

(dp)t~+3- (

P)tx~+~]

/[:el+4 = /[x]+s -- di:el+Z -- d~izl+z,

(Ir) t[xl+s]+l

=

(Ir) trzl+aj

-- (dr)[tz]+sl -- (dr)Tt~]..~l •

Since dt,l+a--

(dp)t,.l.¢4 +

(dr)it,~+aj+x +

(dr)tt,~+4j

for both deaths and

withdrawals, then

qtzl+41rz]+4 = (qP)[z]+a(lP)

[.z]+4 "3i-

qt,+3l+l(lr)[tz/+3/+l

-~

qtz+41(lr)[[z]+4]

,

because (qr)tt~l+31+~ = qt~+~l+~ and (qr)tt~l+41 = qt~+41. We then solve for

(qP)t~-~, which is the only unknown.

Third,

d to ,

(lr)tr=j+z I

= 0.2[(lp)[,]+a-

(dp)[x]+4 -- (

P)b~]+4]

d to ,

(lp) t,~+~

= 0.8[(lp) t,~+4 -

(dp)t,~+4

-- (P) t,1+4]

/[zl+s = /[z1+4 -- d[xl+4 -- d~[zl+4 ,

rto

(lr)

~t~l+4]+t =

(lr)tt~]+41

--

(dr)t[~l+4l

-- (d)tt=l+4l ,

(lr),t.j+31+~

=

(lr)t~,j+31+l

--

(dr)tt,j+sj+x

-- (dr)Tt,l+3l+x •

Since dt.l+ 5 = (dP)t~l+5 + (dr)tt.]+~l+l + (dr)tiz]-~]+2 + (dr)ttx]+5] for both

deaths and withdrawals, then

qt,l+~l[~l+5 =

(qP) t,l+s(lP)

t~]+5 +

qv,+4l+l(lr) tt~]+4l+a

+ q[~+~+~(lr)

t[~]+~+~ + qt~+~l

(lr)t[~l+~

•

We then solve for (qp)[,]+n, which is the only unknown.

Fourth, for l >_ 6,

(Ip)t,]+, = (lp)v~l+t-x- (dp)[~l+t-x- (dp)~,l+t-~,

(lr)[t~l+4]+t-4 = (lr)[t,~]+4]+t-~- (dr)[[zl+4]+t-s-

(dr)7[~]+,l+t-~ ,

(lr) tt~l+z~+t_z

=

(lr) tt~]+z]+,_4

--

(dr) tt,l+al+t_4

--

(dr) t~+z~+,_,

,

556 SELECT AND ULTIMATE RENEWABLE TERM

Since d[.]+, ---

(dp)t.j+t + (dr)tt.j+51+e-6 + (dr)H.j+tj+t-4 + (dr)tr.)+aj+t--.

for both deaths and withdrawals, then

qr.J+,/r.)+, =

(qP)1.1+ t(Ip)[.j+,

+

(qr)

rr.J+sj+,-5(/r) r~.l+5~+t-5

+ (qr)tt.i+4]+,-,t(lr)ft~1+aI+,-,t + (qr)tt.~+a1+,-a(lr)tt.~l+zl+,-z.

Fifth, again, for t > 5 + (pricing mortality select period),

q~,j+, =

(qP)t~+t = q,+,.

We are now in a position to develop a generalized formula. Let

qrizl+t_ t

be the proportion reverting (all of whom are assumed to be standard),

and let

q'~x]+t-t

be the normal aggregate ART lapse rate (t = duration

since original issue). Note that we are assuming that

qt~l+t-x

depends

only on duration since original issue at age x for all persisters and revert-

ers arising from that issue age. We are also assuming that all lapses

occur at year-end and that lapses and deaths are independent.

We can then solve for

(qP)t,l+t

as follows:

t

qt.l+tl[.]+, = (qp)t~]+~(lp)t.l+t + ~ qtt~l+.l+t-~(lr)ir.l+.l+t-. ,

n=l

where

and

t-1

w

l[.1+, = lt.1 II(1 - qt.l+. - qt.l+.).

t-I

(lP)I.l+t /t.lII(1

"

1 '* ,

= - qE.1+.)[ - (q/')~.l+. - q[.J+.]

where

(qp)~

= q~.l; and

n~2

a~O

n--1

X 1 -- (qP)t~l+, -- qfxl+,

*=0

t--n--1

× 1 u I, •

#=0

Until experience develops on this product, estimates of percentages

reverting will necessarily be guesses, but the underwriting department

might be able to give some assistance in estimating the percentage of

potential reverters who would still be standard risks at given ages and

durations. An alternative, albeit complicated, method of ascertaining the

SELECT AND ULTIMATE RENEWABLE TERM 557

proportion of persisters who are still standard at a given duration

might be to apply the techniques developed by Richard Ziock in his

paper "Gross Premiums for Term Insurance with Varying Benefits and

Premiums"

(TSA,

XXII, 19).

It probably would be advisable to price S/U ART using two or three

scales of reversion rates. Any such scale probably should have a relative

or absolute maximum for the policy year given in the policy form for

reversion, since both the agent and the insured have a financial incentive

for reversion at that duration. In that year, regardless of the premium-

paying mode, total lapses (which equal aggregate ART lapses plus

reversions) would be skewed toward the end of the year, since all rever-

sions would tend to occur at year-end, Figure 1 shows some of the

possible total lapse patterns that could be assumed. Pattern A assumes

total lapse rates equal to those under an aggregate ART product (that

is, no reversions) until duration 5, when reversions of 50 percent are

assumed. Pattern B assumes the same reversion rate at duration 5 as

Pattern A, but with additional reversions in years 1-4. Pattern C

assumes that the largest reversion rate will occur in year 3, in spite of

the five-year select period, with another large block of reversions at the

end of year 5.

0,6

0.5

0.4

0,3

0.2

0,1

0.0

I I f I I I l

1 2 3 4 5 6 7

Policy Year

Fro. 1.--Possible total lapse rate patterns for S/U ART

558 SELECT AND ULTIMATE RENEWABLE TERM

Conversions and Conz,ersion Single Premiums

Our conversion rate assumptions for S/U ART did not differ from

those used in pricing an aggregate ART product. An argument could be

made for using somewhat higher conversion rates in the ultimate years,

since the differential between the premium for a standard permanent

product and the ultimate S/U ART premium (which for our product was

equivalent to a low substandard aggregate ART premium) might be

small enough to induce extra conversions.

We also made the debatable assumption that the mortality of people

converting their S/U ART to a permanent plan of insurance would be

no higher or lower than the mortality of those continuing with the S/U

ART product. This assumption is consistent with our pricing of other

term plans. Our reasoning was that the S/U ART is renewable well

beyond the last conversion date, at rates significantly below those for a

permanent plan; hence it would be cheaper for an insured in very poor

health to hold onto the term product. Naturally there are gray areas--

people who are in poor health but who are not on their deathbeds might

feel that they should convert while they still have the chance. The

healthier members of the group, however, could equally well decide that

they want permanent coverage, and exercise their conversion options.

In any event, until the duration t is such that (qP)c~]+t = qc~+~ (that is,

while t >_ (S/U ART select period) + (select period in pricing mor-

tality table), the above mortality assumption produces much higher

ultimate-year conversion single premiums (CSPs) than one obtains for

an aggregate ART product. These high CSPs can have a significant

effect on profits or premium levels in the ultimate years. One possible

solution would be to limit the convertibility of S/U ART to the select

years only. To ignore the conversion cost is to assume that the extra

conversion mortality will be borne by the conversion product, which

therefore should be priced accordingly.

Expenses

It is important to account for any extra selection expenses expected in

the year of reversion guaranteed by the policy. One would expect that

virtually everyone would ask to be underwritten if the financial incentive

were great enough (and it probably is for our product, since the company

pays the cost). As a result, the company would expect to incur medical

and inspection costs for nearly the entire group of insureds at that dura-

tion, but only those who are still standard can revert to a new select

rate. Those who revert are priced as new issues; their underwriting

costs will be more than compensated for, because it is reasonable to

SELECT AND ULTIMATE RENEWABLE TERM 559

suppose that all who qualify as standard risks will revert, and because

new-issue underwriting costs are inflated by the not-taken and declination

rates. Thus, in accounting for extra selection expenses, the real question

is whether the percentage of those applying to revert who are not stan-

dard (and thus not allowed to revert) is greater than or less than the

usual not4aken rate for new issues. An additional expense need be

added in the pricing only if it is expected that more people will be declined

for reversion than would decide not to take the policy if they were new

first-time applicants.

Equity

A very real question of equity arises if persisters are required to

amortize acquisition expenses incurred by reverters. In any plan of

insurance, those who continue under the plan are burdened with the

acquisition expense of those who lapse in the early years. However, under

an S/U ART product, this condition is aggravated by the contractual

provision allowing reversions and by commission and premium scales

that encourage reversions before the point called for in the contract.

One approach to this problem would be to discourage early reversions

by making reversions less attractive to the agent. This might be ac-

complished by paying a level commission during the select years. Since

the agent's commission (as a percentage of premium) would be the same

whether the insured continued on the select scale or reverted early,

the agent's incentive to seek early reversions might be reduced. Alterna-

tively, the company could agree to pay only a renewal commission in

cases of early reversion. This also would reduce the incentive to the

agent to seek early reversions, but it would require that the company be

able to detect them. Under this approach, the savings realized by not

paying a full first-year commission for those who revert early would be

used to offset the unamortized original acquisition expense that the

early reverters would otherwise leave behind for the persisters to absorb.

(It is assumed that such savings arise because premiums were calculated

on the basis of full first-year commissions.) An extension of this idea

would be to pay a reduced commission on all reversions, whether early

or not.

Another approach would be to make early reversions less attractive

to the insured. One could require the insured to supply satisfactory

underwriting evidence at his expense in order to apply for a contractual

reversion or an early reversion. Here again, if rates were calculated

assuming full underwriting expenses, the savings could be used to offset

the amount of unamortized initial acquisition expense. This approach

560 SELECT AND ULTIMATE RENEWABLE TERM

might also reduce the number of those seeking to revert. Alternatively,

one could design an S/U ART product with level premiums during the

select period. This would eliminate the incentive to revert early, since

the level premium rate would be higher for higher issue ages.

Unfortunately, many of these proposed solutions may not seem very

practical in the current marketplace. Reducing commissions to the agent

on contractual or early reversions could well result in having reversions

placed with other companies that pay full first-year commissions on new

lives; the company then would realize no savings with which to offset

unamortized acquisition expenses. A similar result might follow from

having reverters pay for their own underwriting. Designing a product

with level select-year premiums is an intriguing idea, but the product

might not be attractive to insureds who can obtain a lower rate in the

early years by purchasing a nonlevel select-year premium product.

Despite these problems, it is the authors' belief that some of the above

measures should be instituted in order to emphasize to agent and insured

alike that early reversions are not desired by the company.

If we assume that some control can be exercised over early reversions,

one further point should be stressed: it is important to preserve equity

between those who revert contractually at the end of the select period

and those who persist beyond the select period. This can be accomplished

in the pricing process by making sure that the asset share at the end of

the select period is sufficient to generate a percent-of-premium profit

roughly equal to that which will be contributed by the persisters over

the expected lifetime of the policy.

Profits

Because of the many uncertainties about the magnitudes of the major

variables needed to price this product, it seems reasonable that one

would want higher than normal profit margins built into the premiums.

Further, we felt that the asset share should be positive at the end of the

select period, even for the most pessimistic lapse assumptions.

Calculation of percent-of-premium profit to be earned over, say,

thirty years for a closed block of new, first-time issues is complicated

by the fact that the policy provides for reversion at the end of the select

period, as indicated in Figure 2. It should be noted that Figure 2 assumes

that reverters before the end of the fifth year (the date the contract

allows reversion) are really lapses and do not contribute to profits.

Let us define the following:

(AS)t,1+, = Asset share per unit in force at the end of policy year t for

issue age x;

SELECT AND ULTIMATE RENEWABLE TERM 561

P~ul+~

= Probability of reverting at the end of a policy select period

of five years;

pr = Probability of surviving all decrements for a t-year period

t [~t

for someone aged y at issue; and

*rt.j+t -- Accumulated premium dollars per unit in force.

Then the total asset share per unit in force after thirty years attributable

to a new issue at age x is

T R I

( AS)~j+3o + ~P[,]P[,I+.~( A S)

[,+sj+~5

T R

q'- sP[~lPf~l+5 +P'~,+51P'~+sI+~( AS)'[~+xol+~o

T R tT tR t

+ • • • + 5PromPt.I+5 • • • 5P c.+2o]P r.+2o]+5(AS) c~+25]+5,

where the primes indicate that the lapse assumptions entering into the

computations for those who have reverted at least once may differ from

the lapse assumptions used for new issues. For instance, in the first five-

year period, lapses might be greater than those given by a blended

pricing assumption pattern; in subsequent (reversion) select periods,

lapses might be expected to be somewhat less than those assumed in the

pricing. Total accumulated premium for the given closed block of business

is computed using the above formula and replacing all

AS's

by 7r's.

JJJ

Years from Original Issue

Y

Fro. 2.--Asset shares for S/U ART

562 SELECT AND ULTIMATE RENEWABLE TERM

Ultimate Premiums at Ages beyond the Last Allowed Reversion Age

If the policy is renewable beyond the last age for which the insured is

allowed to revert, then the ultimate premiums for ages beyond the

maximum reversion age should reflect the fact that the group of insureds

paying these ultimate rates includes an increasing number of standard

risks. If the maximum issue age and maximum reversion age coincide,

then, from the end of the last premium select period onward, one might

expect mortality about equal to that for an aggregate product with the

same maximum age at issue.

ADMINISTRATION AND EXPERIENCE MONITORING

Since lapses have such an impact on mortality rates and expense

amortization, they must be monitored carefully and discouraged when

possible. One question that is certain to arise is, "What do you do if an

insured applies for a new select rate before the allowed reversion date?"

Since reversions are treated as lapses in the asset share, this behavior

increases lapse rates. Our company will not pay the agent a first-year

commission on a new policy resulting from a reversion before the end

of the select period. However, this system is not foolproof; in a brokerage

agency, for example, the broker could have the insured switch back and

forth every year or two between two companies offering S/U ART

products. The insured would get low rates and the agent would pile up

first-year commissions. Discouraging these frequent replacements would

seem to be very difficult. Policies with level premiums and level com-

missions in the select period probably would help a great deal, as would a

good program to detect twisting. A company could also emphasize the

possible disadvantage to the insured of starting a new contestable period

with each replacement.

Although reversions are treated as lapses, it would be useful, for

purposes of refining the pricing assumptions, to know what proportions

are reverting. One also would need to know (a) how many reversion

medicals the company is paying for, as compared with the number

reverting and (b) the usual not-taken rate,

CONCLUSION

We hope that the techniques and considerations presented in this

paper give actuaries some useful ideas for pricing S/U ART and an

awareness of the very real dangers inherent in marketing these kinds of

plans. Emerging lapse experience will take much of the guesswork out

of estimating reversion rates and thus will improve the accuracy of

future pricing. Meanwhile, in our opinion, the best policy would be to

SELECT AND ULTIMATE RENEWABLE TERM 563

price defensively by designing the plan so that there are few incentives

for early reversion. Some of the defensive measures mentioned in the

paper may be hard to market. Given the reversion feature in the con-

tract, the development of ultimate-year mortality rates based on as-

sumed reversion rates is of primary importance. It is the authors' con-

clusion that, because of this reversion feature, ultimate-year premiums

should be substantially higher than either select-year rates or aggregate

ART premiums.

ACKNOWLEDGMENTS

Several useful suggestions were made by the reviewers. Early in our

pricing work, Steve Lewis made a couple of key observations on the

notion of conservation of total deaths. We would also like to thank

Ken Mihalka for his efforts in writing the program to calculate the

modified mortality rates appearing in Appendixes I and II.

APPENDIX I

AGGREGATE ART MORTALITY COMPARED WITH S/U

ART PERSISTER MORTALITY: ALL

REVERSIONS AT END OF YEAR 5

(Issue Age 45)

DURAl'ION

SINCE

Iss~

0 .........

1 .........

2 .........

3 .........

4 .........

5 .........

6 .........

7 .........

8 .........

9 .........

10 ........

11 ........

12 ........

13 .......

14 .......

15 .......

16 .......

17 ........

18 ........

19 ........

20 .......

21 .......

22 .......

23 .......

24 .......

25 .......

26 ........

27 ........

28 ........

29 ........

MORTALITY RATE PER 1,000

Aggregate S/U ART

ART Persister

Mortality Mortality

(i) (2)

1.70 1.70

2.36 2.36

2.99 2.99

3.59 3.59

4.12 4.12

4.66 7.00

5.23 7.01

5.85 7.20

6.53 7.54

7.48 8.43

8.51 9.57

9.68 11.00

11.02 12.72

12.55 14.71

14.34 17.10

16.50 19.98

MODIFICATION

TO AGG~GA~

ART

MORTALITY

1[(2)--(1)1/(1)1

0.0

0.0

0.0

0.0

0.0

50.2

34.0

23.1

15.5

12.8

12.4

13.6

15.4

17.2

19.3

21.1

18.01 21.16

19,69 22.25

21.63 23.48

23.81 24.80

26.17 26.17

28.73 28.73

31.40 31.40

34.21 34.21

36.99 36.99

39.92 39.92

43.46 43.46

47.47 47.47

51.73 51.73

56.43 56.43

17.5

13.0

8.6

4.2

0.0

0.0

0.0

0.0

0,0

0.0

0.0

0.0

0.0

0.0

PERCENTAGE

REVERTING

o%

0

0

0

0

50

o

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Non~.--Test calculations using an underlying lapse rate equal to that for aggregate

ART and using an underlying lapse rate of 0% produced mortality rates only slightly

different from each other.

564

APPENDIX II

AGGREGATE ART MORTALITY COMPARED WITH S/U

ART PERSISTER MORTALITY: REVERSIONS AT

END OF YEARS 3, 4, AND 5

(Issue Age 45)

DURATION

SINCE

Issue

0 ........

1 ........

2 ........

3 ........

4 ........

5 ........

6 ........

7 ........

8 ........

9 ........

10 .......

11 .......

12 .......

13 .......

14 .......

15 .......

16 .......

17 .......

18 .......

19 .......

20 .......

21 .......

22 .......

23 .......

24 .......

25 .......

26 .......

27 .......

28 .......

29 .......

MORTALITY RATE I~ER 1,000

Aggregate S/U ART

ART Persister

Mortality Mortality

(1) (2)

1.70 1.70

2.36 2.36

2.99 2.99

3.59 4.25

4.12 4.89

4.66 5.96

5.23 6.19

5.85 6.56

6.53

7.10

7.48 8.20

8.51 9.43

9.68 I0.81

II .02 12.43

12.55 14.25

14.34 16.37

16.50 18.96

18.01 19.96

MODI ]¢ICATION

"~o AGGREGATE

ART

MORTALITY

I[(2)-(i)I/(D I

0.0

0.0

0.0

18.3

18.8

28.0

18.4

12.1

8.8

9.6

10.8

11.7

12.8

13.5

14.1

14.9

10.8

19.69 20.97

21.63 22.20

23.81 24.05

26.17 26.17

28.73 28.73

31.40 31.40

34.21 34.21

36.99 36.99

39.92 39.92

43.46 43.46

47.47 47.47

51.73 51.73

56.43 56.43

6.5

2.6

1.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

0.0

PERCENTAGE

REWarlh'O

0%

0

0

30

10

20

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

0

Nozz.--Test calculations using an underlying lapse rate equal to that for aggregate

ART and using an underlying lapse rate of 0% produced mortality rates only slightly

different from each other.

565

DISCUSSION OF PRECEDING PAPER

TO~[ BAKOS:

One reason for the development of a select and ultimate annual renew-

able term (ART) product that was not mentioned by the authors is to

minimize deficiency reserves. Although the expression "deficiency

reserve" is not used in the 1976 amendments to the standard valuation

law, additional reserves equivalent to what used to be called deficiency

reserves are still required if an ART gross premium is less than some

statutory minimum. These additional reserves can be minimized by

establishing the ultimate premiums of a select and ultimate ART product

at a level that is not deficient. Competition demands, and experience

mortality permits, select premiums much lower than ultimate premiums.

These select premiums probably would be deficient. If the select period

were five years, the anticipated premium stream would consist of select

(probably deficient) rates for the first five years and ultimate (non-

deficient) rates thereafter. Deficiencies would be limited to the first five

policy years, not the entire renewal period, producing a significantly

smaller surplus strain than would be produced by the alternative, a com-

petitive aggregate ART product.

To make what would otherwise be a very uncompetitive product com-

petitive, the reversion feature is added, which allows insureds to re-

qualify for the select rates as described in the paper. Those companies

that adopt a select and ultimate premium structure only as a gimmick

to avoid large deficiency reserves probably would impose minimal under-

writing requirements so as to requalify nearly 100 percent of their policy-

holders at each requalification period. Such companies would have what

the paper describes as aggregate ART products disguised as select and

ultimate products. Those companies that approached the select and

ultimate product more naively and attempted more serious underwriting

would requalify something less than 100 percent and would incur

significant additional expenses that would increase the price of the

product. Both types of companies would lose the competitive advantage

of guaranteed low rates throughout the renewal period. In this sense, a

select and ultimate reversionary product is not as competitive as an

aggregate guaranteed premium product.

Although there may have been other needs that caused the develop-

ment of a select and ultimate ART product, the need to minimize de-

567

568 SELECT AND ULTIMATE RENEWABLE TERM

ficiency reserves was the first that I became aware of, and it is reasonable

to suppose that these other needs developed in an effort to legitimize the

concept. Certainly the need to reduce deficiency reserve requirements

has stimulated other forms of product innovation. For example, we also

have guaranteed maximum premium ART products and participating

ART with an ultimate premium rate structure after, say, the third year.

The dividends for this participating ART begin at the end of the third

year and are mysteriously equal to the difference between the ultimate

and the initial-scale premium.

Another approach to pricing a select and ultimate ART product is

described in the remainder of this discussion. This alternative approach

starts with the principle of conservation of total deaths described in the

paper, but limits its application because mortality and persistency are

felt to unfold in a manner different from that assumed in the paper.

Basic Approach

Take the paper's basic formula that expresses the principle of con-

servation of total deaths at the requalification age [x] + 5,

qi,l+~lt,~+~ = (qP) txl+~(lP)r,l+~ + (qr) trxl+51 (lr) tt,l+51 ,

and rearrange it as follows:

(/r)tt,l+sl

(qr)cf,~+5 T +

(/P)[~1+5

(qp)f,~+5.

qfx]+~ --- /fx]+5 lrxl+5

We know that lt.l+s = (lr)ttxl+~l + (/P)t~l+5, so we can make the following

definitions:

(lp)~.I+5

(/r)c~I+sl and 1 - k~,j+~ =

kr'l+5 = lt~1+5 I[,1+~

where kt~l+5 is the proportion of the age x issues reverting at age Ix] + 5.

Substituting in the rearranged formula yields

qE~]+.~ =

k[xl+~(qr)ttx]+~l +

(1 - kf~l+~ ) (qP)t~l+~,

which we can solve for ki,l+~ as follows:

(qP)t.l+5 - qI,l+~

k[,]+~ =

(qP)c,~+5 -- (qr)~c~+sl "

In their paper Dukes and MacDonald assume that the proportion revert-

ing is 50 percent and then solve for the persister mortality,

(qp).

They

have also assumed that the reverter mortality,

(qr),

is equal to new

select mortality. Their solution for

(qp)

beyond duration 5 depends on

the assumption that lapse rates for the persister and reverter classes are

DISCUSSION 569

identical and that total lapses are the same as for an aggregate ART

product. This assumption seems questionable. The reverters, through the

reselection process, have been determined to be standard. The persisters,

then, are obviously substandard, and the ultimate premium they will be

charged includes, implicitly, a substandard extra. Presumably, under

an aggregate premium structure none of these persisters would have

lapsed for another ART product, since it would be available to them

only on a substandard basis. Why give up a standard rate for a sub-

standard rate? These same persisters, however, when charged an ulti-

mate, implicitly substandard premium, would be prompted to shop.

Those better substandard risks in the persister class probably would be

successful in finding a better aggregate ART rate, even if it were sub-

standard, and they would lapse their policies.

The reverse of this argument could be made for the reverter class, and

it could be asserted that their persistency will be better than that for an

aggregate product. Thus, it is logical to assume that persistency for the

reverter class would be different from that for the persister class and

that, in total, persistency would be different from aggregate ART

persistency.

It should be noted that the persister mortality is just as dependent

upon the assumption made for the proportion reverting as it is upon the

lapse assumption. This was demonstrated in the paper. If these assump-

tions cannot be made reliably, then the persister mortality cannot be

solved for reliably. There is, therefore, no particular advantage in

approaching the problem in this way. Instead, one could establish an

assumption about the level of persister mortality consistent with the

reselection effort planned and the substandard mortality expected, and

then solve for kE,l+5 , the proportion of the age x issues reverting. Thus,

the ultimate ART rates could be set in much the same way that sub-

standard premium rates are set. Knowing the mortality levels under-

lying the ultimate ART rate structure and using ktxl+5 as a guide, the

underwriter could classify the risk as either a reverter (standard) or a

persister (substandard).

In solving for kt.l+6 , the additional assumption would be made that

(qr)cExl+51 = q~+53,

as was done in the paper, and the formula would

become

(qP)M+~ -- q~l+5

All of the assumptions made to solve for kc,j+6 would be made only with

respect to the duration in which the reversion occurred. The value of

570 SELECT AND ULTIMATE RENEWABLE TERM

kt~l+5 would be useful only as a guide in evaluating the reselection

process.

Mortality Assumption

In solving for persister mortality,

(qp),

the paper invokes the con-

servation-of-total-deaths principle, assumes that lapse rates for reverters

and persisters are the same and are equal to those of an aggregate ART

plan, and assumes that reverter mortality is identical with new select

mortality. Under these assumptions, persister mortality and reverter

mortality are related as shown in Figure 1. The curve labeled q shows

the original-issue select and ultimate mortality assumption. The curves

(qp)

and

(qr)

show persister and reverter mortality equaling ultimate

mortality fifteen years after the reversion period.

However, the assumption that reverter and persister mortality each

equal ultimate mortality fifteen years after reversion seems to be only a

pricing convenience. The conservation-of-total-deaths principle is not

infringed if we assume that persister mortality is always greater than

ultimate mortality and that reverter mortality is always less than ulti-

mate mortality, as shown in Figure 2. This assumption seems reasonable

because the reselection process can be expected to weed out the poorer

risks each time it is exercised on the prior reverter class. The reverters

q

I~ ~elect period ~l I

I I

i i

FIO. 1.--Relationship of persister, aggregate, and reverter mortality assumed in

paper.

DISCUSSION

57 l

I " select period : I I

I I

J I

FIG.

2.--Relationship of persister, aggregate, and reverter mortality assumed in

discussion.

remaining after continual reselection might exhibit new select mortality

at the time of reversion, but this select mortality might wear off more

slowly than in an aggregate select class and might settle at a level lower

than aggregate ultimate mortality. Thus, the reverter class can be as-

sumed to be superselect in the sense that the select period it exhibits is

longer than the select period normally assumed in pricing aggregate

ART. To preserve the conservation-of-total-deaths principle, the per-

sister mortality would have to be always greater than the aggregate

ART's pricing mortality. This is consistent with the concept that per-

sisters are really substandard risks.

The formula presented in the paper and modified in this discussion

gives a relationship among

k, q, (qp),

and

(qr)

that holds at all durations

only under the lapse assumption made in the paper. If this lapse assump-

tion is assumed not to hold, then the relationship among these four terms

is not so simple. The complexities of this relationship can be avoided by

assuming that reverter and persister mortality (and persistency) are

independent of each other.

If a requirement of a select and ultimate product is that deficiency

reserves be minimized, then ultimate premiums for the lowest premium

band or class should not be less than 1,000c, computed on the Modern

572

SELECT AND ULTIMATE RENEWABLE TERM

CSO Table at 4½ percent. This would eliminate deficiencies during the

ultimate period in most states. For pricing purposes, the mortality under-

lying these ultimate rates could be estimated in two ways.

Method 1.

The ultimate premium could be "unloaded." Aggregate ART premi-

ums from a current product could be compared at each age with the average

pricing mortality rate for that age to compute a "load." This "load" could

then be applied in reverse to estimate the persister mortality underlying the

chosen ultimate premium.

Method 2.

The substandard rating implied by the chosen ultimate premium

could be determined by relating the ultimate premium to a current aggregate

ART premium. The percentage extra mortality implicit in the ultimate

premium could then be multiplied by the average aggregate ART pricing

mortality rate for each age to estimate the persister mortality underlying the

chosen ultimate premium.

Table 1 shows the solution for the underlying ultimate mortality using

method 1, and Table 2 shows the solution using method 2. The results,

given the crudeness of the processes, are similar and show that the maxi-

mum substandard mortality occurs at age 30 at about the table 4 (200

percent of standard mortality) level. One might want to modify these

underlying rates for two reasons: First, at the higher attained ages they

are less than the ultimate pricing mortality used for the aggregate ART,

and, second, the implied substandard ratio is not level by age.

TABLE 1

C.4LCULATION OF UNDERLYING

ULTIMATE

MORTALITY USING METHOD 1

Age

(~)

15 ...........

20

...........

25

...........

30 ...........

35

...........

40 ...........

45 ...........

50 ...........

55 ...........

60 ...........

65 ...........

70 ...........

Ultimate

Premium

1,000cx

Modern CSO

44%

(2)

1.30

1.68

1.92

2.03

2.27

3.02

4.41

6.67

10.38

16.07

26.78

41.89

Unloading

Ratio*

(3)

0.45

0.45

0.46

0.42

0.50

0.56

0.62

0.64

0.62

0.52

0.42

0.40

Underlying

Ultimate

Mortality

[(2)X(3)1

(4)

0.59

0.76

0.88

0.85

1.14

1.69

2.73

4.27

6.44

8.36

11.25

16.76

Average

Aggregate

Pricing

Mortalityt

(5)

0.52

0.52

0.49

0.45

0.64

1.07

1.87

3.03

4.80

7.06

I0.53

16.10

Implied

Substandard

Ratio

[(4)/(5)]

(6)

1.13

1.46

1.80

1.89

1.78

1.58

1.46

1.41

1.34

1.18

1.07

1.04

*The unloading ratio for each age is the ratio of average prieingmortality to the lowest

premium band

rate,

t This is a weighted average or "aggregate" pricing mortality at each attained age, which recognizes

the distribution of in-force by duration at each attained age.

DISCUSSION 573

TABLE 2

CALCULATION OF UNDERLYING ULTIMATE MORTALITY USING METHOD 2

Age

(1)

15 ..........

20 ..........

25 ..........

30 ..........

35 ..........

40 ..........

45 ..........

50 ..........

55 ..........

60 ..........

65 ..........

Ultimate

Premium

1,000cz

Modern CSO

(2)

1.30

1.68

1.92

2.03

2.27

3.02

4.41

6.67

10.38

16.07

26.78

Aggregate

ART

Standard Rate

(3)

1.03

1,03

1.03

1.03

1.23

1,85

2,90

4,57

7,49

13.11

24, 19

Implied

Substaudard

Ratio*

~1[(2)I(3)-- I]/

o.91+~11

(4)

1.29

1.70

1.96

2.08

1.94

1.70

1.58

1.51

1.43

1.26

1.12

Average

Aggregate

Pricing

Mortality

(5)

0,52

0.52

O. 49

O, 45

0,64

1.07

1,87

3.03

4.80

7.06

10.53

Underlying

Ultimate

Mortality

[(4)x(5)]

(6)

0.67

0.88

0.96

0.94

1.24

1.82

2.95

4.58

6.86

8.90

11.79

* Our company's substandard ART premiums are calculated by the following formula:

Substandard premium

= P[O.9(r -

1) + 1],

wbere P is the standard ART premium and r is the substandard ratio (e.g., for table 2 substandard mor-

tality, • = 1.5). The values in col. 4 v~re obtained by solving this equation for r.

In Table 3, kt~l+s, the proportion reverting five years after issue, is

calculated assuming that persister mortality is equal to table 4 (200

percent) substandard mortality. The value of k is fairly uniform by age,

indicating that about 70 percent of the in-force would revert under these

assumptions. That is, at the time of reversion the underwriting process

would have to be efficient and precise enough to select the 30 percent

of the total persisters and reverters who will be persisters with an average

mortality equal to table 4. This selection probably would have to be

made knowing that some risks placed in the persister class would lapse

rather than pay the higher ultimate premium. Therefore, the under-

writing target might be to select the, say, 50 percent that average

table 2 substandard mortality.

Other Pricing Assumptions and Profits

Under the approach suggested in this discussion, the lapse assumption

should reflect the expected additional lapses that probably would occur

as insureds lapse their policies rather than accept the ultimate rate. The

expense assumption, as pointed out in the paper, would have to include

the extra selection expenses in the year of reversion. With higher than

normal profit margins built into the product as the authors suggest, the

asset share will be positive at the end of the select period. This would

574 SELECT AND ULTIMATE RENEWABLE TERM

TABLE 3

CALCULATION OF IMPLIED kfzl+s

Aggregate Persister

Reverter

kltT+5

Age

Select Mortality Mortality

{[(2)-- (I)]/

x+5

Mortality

(qP) [~l+5 I(2)- (3)]]

t ,000 qtzl

+4,

[ 2 X (1) ] 1,000qlx+~l

(1) (2) (3) (4)

15

...........

20 ...........

25 ...........

30 ...........

35 ...........

40 ...........

45 ..........

50 ..........

55 ..........

60 ..........

65 ..........

70 ..........

0.52

0.52

O. 49

O. 45

O. 64

1.07

1.87

3.03

4.80

7.06

10.53

16.10

1.04

1.04

0.98

0.90

1.28

2.14

3.74

6.06

9.60

14.12

2l .06

32.20

0.33

0.39

0.32

0.37

O. 46

0.68

1.04

1.47

2.10

3.35

5.68

7.24

O, 73

0.80

0.74

0.85

0.78

O. 73

O. 69

O. 66

O. 64

0,66

0.68

0~65

NoTE.--Persister mortality

(qp),

is assumed to be equal to 2 times

the average

aggre-

gate pric ng mortality, which is assumed to

be equal to q~zl+s, the fifth-year select

pricing

mortality.

assure amortization of initial selection expense before the first reversion.

In this situation, the authors suggest that the extra selection expense

can be equated to the initial selection expense, with the reverters equiva-

lent to new issues and the persisters equivalent to not-takens. They

state that

"an

additional expense need be added in the pricing only if it

is expected that more people will be declined for reversion than would

decide not to take the policy if they were new first-time applicants." It

seems, however, that some additional "expense" has been implicitly in-

cluded in the price of the product in the form of higher profit margins

and the expectation of a positive asset share at the end of the select

period (five years in the example). If persisters are greater in number than

not-takens, even

more

additional expense would need to be incorporated

if it were expected that the reverter class would amortize all the reselec-

tion underwriting expense, including that of the persisters who were

declined for reversion.

Marketability of Select and Ultimate ART

Common sense should indicate that the extra selection expense and

the additional first-year compensation associated with reversion under a

select and ultimate ART product would make it more costly than an

otherwise similar aggregate ART product. When we considered intro-

duction of a select and ultimate ART product as a means of reducing

DISCUSSION 575

our deficiency reserve requirements, we found that we could not com-

pete with our own recently introduced aggregate ART product.

The nonguaranteed nature of the renewal premiums is a significant

problem for select and ultimate ART products. Everyone, no doubt,

thinks he will qualify for reversion; however, the assumptions used in

this discussion indicate that 30 percent will not, and in the paper it was

assumed that 50 percent will not. These nonqualifiers will be expected to

pay the higher ultimate premiums. As each reversion period passes, the

size of the persister class grows. Ten years after issue, there probably will

be more persisters than reverters, assuming that the persisters have not

lapsed. After fifteen years, at least two-thirds will be persisters. This

large group of people, by opting for a select and ultimate product, will

have given up the guaranteed standard renewal premiums they would

otherwise be paying for an aggregate ART product.

The nature of a select and ultimate ART would seem to prohibit sub-

standard issues. If, in order to revert, an insured must be a standard

risk, he probably should be standard at issue also. Would a company

that offered only select and ultimate ART be able to insure a substandard

risk?

Summary

The purpose of this discussion was to point out that another approach

to pricing a select and ultimate ART product would be to choose an

appropriate level for the ultimate-year mortality rates and develop the

reversion rates implied by that level of mortality. The discussion was

meant to imply that this would be a more practical way of approaching

select and ultimate ART product development than the procedure sug-

gested in the paper.

JOHN C. GOULD AND ]AMES R. PORTER:

This is a timely paper, since it addresses very real questions in pricing

a currently popular and competitive product. This discussion addresses

questions raised by the authors' observation that lapse rates had little

effect on persister mortality. For their illustrations, the authors assumed

that the same lapse rates applied to the persisters and the reverters.

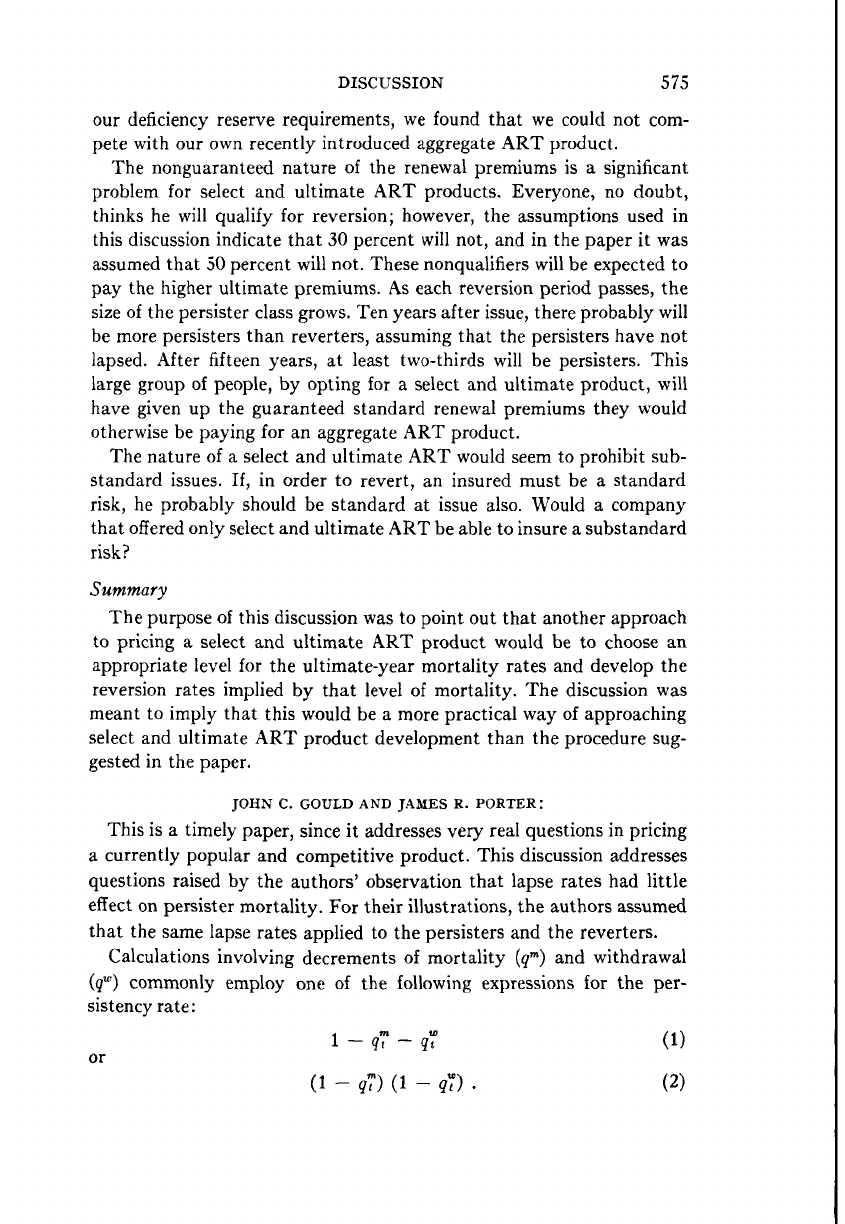

Calculations involving decrements of mortality (q~) and withdrawal

(qW) commonly employ one of the following expressions for the per-

sistency rate:

1 -- q7 - qT (1)

or

(1 - q7) (1 -

qT). (2)

576 SELECT AND ULTIMATE RENEWABLE TERM

If the q's are from a double decrement table (deaths and withdrawals)

and if both decrements apply simultaneously and continuously, then

expression (1) is exact. This expression is used in the paper. However, if

the only q's available are from separate mortality and withdrawal tables,

formula (14.38) from Jordan's

Life Contingencies

can be used to compute

the double decrement rates from the known single decrement rates. The

persistency rate, in terms of the single decrement rates, is given by the

expression

(1 q~)(1 - q~) -

,~'~'~

-

~ ~

(3)

1 ~ 1 /m /w

• qt qt

Expression (2) is a closer approximation to this expression than is ex-

pression (1). To illustrate the difference between these expressions, as-

sume a mortality rate of 2 deaths per 1,000 and a 10 percent withdrawal

rate. The resulting values of the three expressions are

(1) 0.8980; (2) 0.8982; (3) 0.898245.

If the exposure to withdrawal is on premium due dates (as when there

are no cash values) and weighted heavily on the anniversary (as for

annual premiums or annual increases in premium), expression (2) is the

best approximation to the persistency rate. Given this approximation

and the assumption of the same withdrawal rates for persisters and

reverters, persister mortality is independent of withdrawal rates:

(qp)t = qtlt_~(1 -- qt-:) -- (qr)t(lr),_~[1 --

(qr)t_~] " (4)

(lp)t_i[1 -- (qp),_,]

Table I of this discussion compares persister mortality rates computed

using the authors' formula with those computed using the formula above

under various withdrawal assumptions. The assumed basic mortality is

from a five-year select table with select rates equal to the following per-

centages of the ultimate rates (see Table 3): 85 percent in the first year,

then 90, 94, 97, and 99 percent. Reversion rates assumed are 50 percent

of in-force at the end of two years, and 30 percent of persisters in force

at the end of four years.

The first column of Table 1 shows persister mortality rates assuming

no lapses. These will also be the mortality rates assuming equal lapse

rates for reverters and persisters and using expression (2) for the per-

sistency rate.

Column 2 of Table 1 shows persister mortality calculated using the

authors' formulas with a flat I0 percent lapse rate. A comparison of

columns 1 and 2 illustrates the very slight effect of the assumed lapses.

DISCUSSION

TABLE 1

COMPUTED PERSISTER MORTALITY RATES (X|,000)

577

Flat 10% Lapses from Lapses from

Attained Age No Lapse Lapse Table 3 Table 3

(1) (z) (3) (~)

30 ..............

31 ...............

32 ...............

33 ...............

34 ...............

35 ...............

36 ...............

37 ...............

38 ...............

39 ...............

1.8275

1. 9800

2•3175

2. 423266

2. 691554

2.714481

2.756132

2. 836050

3.012877

3. 250

1. 8275

1. 9800

2•3175

2. 423274

2.691568

2.714503

2. 756146

2. 836055

3 •012879

3. 250

1 •8275

I. 9800

2.3175

2. 4775

2. 7923

2.7911

2•7918

2. 843824

3 •015653

3. 250

1.8275

1.9800

2.3175

2. 4669

2. 7488

2. 7802

2. 7892

2. 843854

3.015664

3. 250

NoTz.--Column 3 calculated using expression (1) of this discussion; col. 4 calculated using expression (2).

Columns 3 and 4 show the effect of assuming that the lapse rates from

the withdrawal table are combined rates but that the reverters' lapse

rates are significantly lower. (It could be argued that the reverters have

lower lapse rates because they pay lower premiums, or that the persisters

have lower lapse rates because a significant portion have discovered that

they are uninsurable or are rated risks.) Column 3 was computed using

the authors' formulas, while column 4 uses the expressions in this dis-

cussion. (Lapse assumptions used are shown in Table 3.) Persister lapse

rates, shown in Table 2, were computed in a manner analogous to the

method used for the persister mortality rates.

Our conclusions are as follows:

I. When differing lapse rates can be confidently assumed (from experience) for

persisters and reverters, they should be recognized for their effect on both

mortality and persistency. Until then, it is reasonable as well as convenient

TABLE 2

PERSISTER LAPSE RATES (PERCENT), COMPUTED USING LAPSE RATES

IN TABLE 3, AND EXPRESSIONS (1) AND (2) OF THIS DISCUSSION

30.

31.

32.

33.

34.

Attained

Age

Expression

(i)

0.0

25.0

25.0

12. 5345

15.3813

Expression

(2)

0.0

25.0

25.0

12. 5361

15.3843

Attained

Age

35.

36.

37.

38.

39.

Expression

(1)

., 9. 5864

6. 8450

i I 5.o

.i 5.o

• 5.0

Expression

(2)

9. 5890

6.8466

5.0

5.0

5.0

578

SELECT AND ULTIMATE RENEWABLE TERM

TABLE 3

MORTALITY AND LAPSE ASSUMPTIONS USED IN

THE ILLUSTRATIONS

Ultimate

Attained Mortality Aggregate

Age X 1,000 Lapse (%)

(2) (2)

30 ........

31 .....

32 .....

33 .....

34 .....

35 .....

36 .....

37 .....

38 .....

39 .....

2.15

2.20

2.25

2.33

2.40

2.50

2.65

2.80

3.00

3.25

0.0

25.0

15.0

10.0

9.0

7.0

5.5

5.0

5.0

5.0

Reverter at Reverter at

Duration 2 Duration 4

Lapse (%) Lapse (%)

(3) (4)

5.0 ..........

8.0

7.0 3.0

6.0 6.0

5.0 5.0

5.0 5.0

5.0 5,0

5.0 5.0

to compute persister mortality ignoring withdrawals. Given the computed

mortality table, various withdrawal rates can and probably should be tested.

2. The "conservation of total deaths" concept is a little too handy. It would

not be appropriate to adopt it this early as a generally accepted actuarial

assumption like the time-honored concept of uniform distribution of deaths.

In the meantime, this paper defines an important territory of uncertainty

and begins to map it.

COURTLAND C. SMITH:

Messrs. Dukes and MacDonald have presented a timely and interesting

paper. For the rational, informed consumer in an inflationary environ-

ment, the product is a plus. The select and ultimate annual renewable

term (S/U ART) policy gives low-cost insurance. With reversion, the

customer's options are increased. Given continuing competition, costs can

only come down.

The product would seem to represent a positive development for the

rational, informed agent as well. Caught in the squeeze between declining

first-year commissions and rising living costs, the agent is forced to make

more frequent sales or sell ever larger policies to survive. S/U ART, with

its reversion feature, legitimizes frequent resales to existing customers

who remain in good health.

For the rational, knowledgeable life insurance company, S/U ART

represents an opportunity and a problem. The company needs new busi-

ness to survive, and the product is attractive. S/U ART can help attract

new healthy lives, but the company may not prosper as a result. Much

DISCUSSION 579

existing in-force may simply be rewritten. The business written may not

persist long enough to amortize first-year costs. The proportion reverting

may be greater than anticipated, and both reverters and persisters may

then show much higher mortality than was assumed in the original

pricing. Thus, the Dukes-MacDonald S/U ART product seems espe-

cially vulnerable to lapse by healthy lives at the start of the third, fifth,

and sixth durations, and to renewal by lives less healthy than anticipated

at the start of the sixth and later durations.

The solution to the life company's problem lies in the fact that there

are numerous reinsurance compauies in the marketplace that are willing

to compete aggressively for new business. By coinsuring the lapse risk

as well as the mortality risk at favorable allowances, the direct company

can shift the hazards of S/U ART to the reinsurers and remain confi-

dently competitive. I have heard it said that some term policies being

sold today are profitable only because of the reinsurance.

It seems to me that the most refined form of S/U ART policy would

allow reversion every year. To save underwriting expenses, medical

requirements would be reduced each policy year, except perhaps the

fifth, tenth, fifteenth, and so on. As cases reach their first anniversary,

and the insureds are given the option to revert, the healthiest insureds

are likely to submit evidence first, and very little adverse information

is likely to be found. I think it would be very tempting, given these

early results, for the marketing department to propose that further

requests for evidence be waived in the first year in order to reduce both

expenses and lapses! Interestingly, if the coinsurance conditions are

sufficiently competitive, it could pay the actuary to ask his reinsurers

to agree. And it might be difficult for them to refuse!

I have heard the S/U ART policy described as the first life insurance

product in history designed to self-destruct. In the present market, I

suspect that the policy may survive, but some individual companies

may self-destruct instead.

The property-casualty insurance market is based mainly on sales of

annual renewable term policies having yearly reentry provisions. With

inflation in medical costs and property repair charges, claim costs and

coverage limits tend to rise. Premiums tend to exhibit a roller-coaster

pattern. Premiums increase faster than claims when catastrophic experi-

ence or technological innovation drives excess reinsurance capacity out

of the market, but more slowly than claims when a series of profitable

years draws insurance and reinsurance capacity back in. In the capacity-

contraction phase, it is not unusual for companies to self-destruct or

merge.

580 SELECT AND ULTIMATE RENEWABLE TERM

To some observers, the property-casualty roller-coaster cycle lasts an

average of six to seven years. The life insurance industry has all the signs

of moving in the same direction. If so, I wonder how long the life cycle

will be.

(AUTHORS' REVIEW OF

DISCUSSION)

JEFFER¥ DUKES AND ANDREW M. MAC DONALD:

We were somewhat disappointed that this paper did not generate more

written discussion of the merits, viability, and pricing methodology of

S/U ART products, especially since so many companies are issuing or

reinsuring such plans. However, we did receive three such discussions,

and we wish to thank these contributors for taking the time to put their

thoughts in writing.

Before we examine each discussion separately, we would like to ad-